.jpeg)

New branches on Sequoia’s tree

Something unusual happened this week. Sequoia Capital—arguably the most disciplined venture firm in history—is reportedly joining Anthropic's $25 billion funding round at a $350 billion valuation.

The unusual part: Sequoia already has major positions in OpenAI and xAI, as we mentioned in Tuesday’s coverage. Traditional VC portfolio theory says you don't back three direct competitors. Sequoia's apparent answer: the AI market will be large enough that multiple winners can emerge.

The firm reportedly views this less like picking a winner and more like ensuring access to the entire category. When the AI market is projected to approach $1 trillion by 2027, according to projections from Bain, owning stakes in the three leading foundation model companies starts to look less like a conflict and more like an allocation strategy.

What does this signal for private market investors? The institutional consensus is hardening around a few key beliefs: AI infrastructure companies will continue commanding premium valuations, the market is big enough for multiple scaled winners, and the cost of not having exposure to the category is becoming untenable.

For individual investors, the Sequoia signal suggests these unprecedented valuations reflect considered institutional judgment about the magnitude of what's being built.

AI capital wars: The $25 billion Question

Anthropic's $25 billion funding round started as a $10 billion term sheet, growing as more investors asked in, with Coatue and Singapore's GIC leading at $1.5 billion each, according to CNBC.

The math now:

- Anthropic: $350B valuation, up from $183B in September

- OpenAI: Reportedly preparing for IPO at valuations approaching $1 trillion

- xAI: $230B valuation after $20B Series E closed January 6

The pattern investors should note: AI companies raised over $47 billion in just the first two weeks of January 2026, according to industry reports. This isn't the steady allocation of normal venture cycles—it's institutional capital repositioning around a generational technology shift.

The caution: These valuations assume AI companies can convert hype into durable, recurring revenue. Anthropic is reportedly targeting $20-26 billion in annual revenue for 2026—a significant multiple expansion from reported current levels of around $9 billion. The company is explicitly shifting focus from experimental use to developer tools and enterprise workflows, trying to convert speculative usage into long-term contracts.

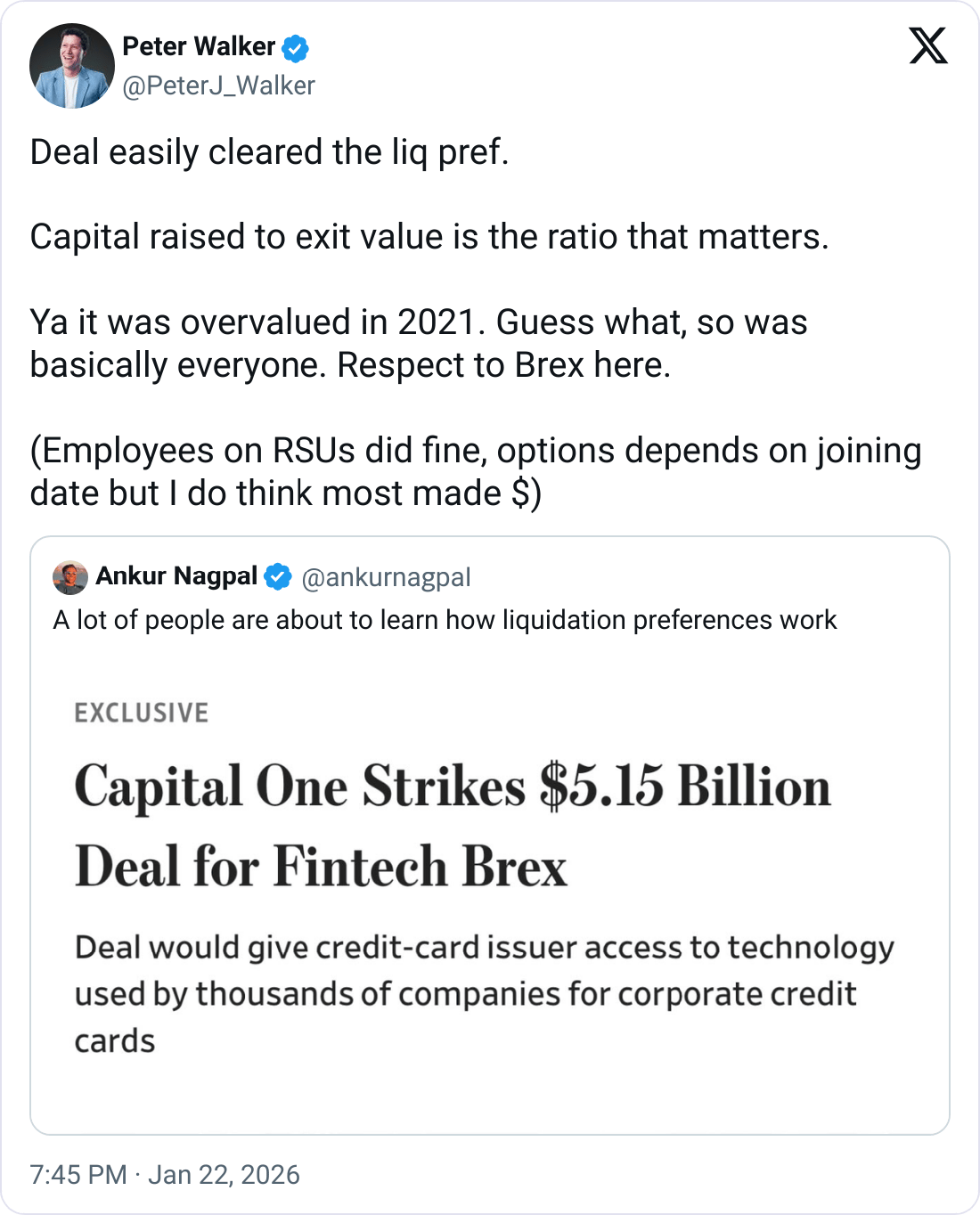

Fintech reality Check: Capital One acquires Brex at 58% discount

Capital One announced Thursday it will acquire Brex for $5.15 billion in a half-cash, half-stock deal—a significant markdown from the corporate card company's $12.3 billion valuation in 2022.

Why it matters: The deal illustrates the valuation reset hitting even successful fintechs. Brex built a legitimate business serving 25,000+ customers including DoorDash, Robinhood, and Anthropic, pioneering the integration of corporate cards, expense management, and banking software. But the 58% haircut from peak valuation reflects the gap between 2021-era multiples and today's acquisition math.

The strategic logic: Capital One CEO Richard Fairbank called Brex's model "the winning offer" for business payments, noting the company had built a "vertically integrated platform from the bottom of the tech stack to the top." Coming less than a year after Capital One's $35 billion Discover acquisition, the deal signals continued appetite for payments infrastructure.

The contrast that stings: Competitor Ramp hit a $32 billion valuation in November 2025 and announced $1 billion in ARR with 50,000+ customers. The divergence between the two expense management platforms shows how quickly market position can shift in fintech.

For private market investors: Early backers like Ribbit Capital, which led Brex's $7 million Series A in 2017, still see substantial returns—estimated at 700x before dilution. But late-stage investors who bought at peak valuations could face meaningful losses, a reminder that entry price matters even for category leaders.

Meanwhile, all of VC Twitter X is arguing about which investors will get their money back first, and at what multiple.

Check out this tweet for as full a cap table breakdown as the general public is likely to get.

Robotics: the next foundation model bet

Skild AI's $1.4 billion Series C at a $14 billion valuation—tripling from $4.5 billion just seven months ago—represents another significant institutional bet on foundation models, this time for physical systems.

What Skild is building: The "Skild Brain" is an omni-bodied foundation model that can control robots without being trained on specific hardware. Think of it as an operating system that works across quadrupeds, humanoids, tabletop arms, and mobile manipulators—with the ability to adapt in real-time to new environments.

Why the valuation moved: Revenue. Skild scaled from zero to approximately $30 million in just months during 2025, the company said, deploying across security, construction, delivery, warehouses, and data centers. Skild isn't just a research lab—it has customers.

The investor lineup matters: SoftBank led, with NVentures (Nvidia's venture arm), Bezos Expeditions, Samsung, LG, Schneider Electric, and Salesforce Ventures participating. When strategic investors from consumer electronics, industrial equipment, and enterprise software all write checks, they're signaling where they expect robots to show up.

The thesis: Robotics has been waiting for its "ChatGPT moment"—when foundation models enable rapid deployment across diverse applications without bespoke training. Skild's claim is that they've built that capability. The next 12-18 months will test whether the model generalizes as broadly as the valuation implies.

Quick takes

New AI lab Humans& raises $480M seed at $4.5B valuation — Founded by alumni from OpenAI, Anthropic, xAI, and DeepMind, the three-month-old company is building "human-centric" AI for collaboration tools. The round underscores continued willingness to fund experienced AI teams at massive pre-revenue valuations.

Zipline closes $600M at $7.6B valuation — The drone delivery company will use funds to expand U.S. operations in Houston, Phoenix, and other markets. Deliveries doubled from 1M to 2M in 2025.

Wellington Management: VC secondaries remain underpenetrated — The firm noted that only about 2% of unicorn market value trades on the secondary market, suggesting significant room for expansion as the asset class matures.

Geopolitical uncertainty weighing on investment decisions — Citadel's Ken Griffin warned at Davos that global trade policy uncertainty is affecting capital allocation across markets.

Data point of the day

58%

The discount from peak valuation at which Capital One is acquiring Brex. The $5.15 billion deal versus Brex's 2022 valuation of $12.3 billion illustrates the recalibration hitting growth-stage fintechs with pandemic-era funding rounds, as acquirers apply traditional M&A math rather than venture multiples.

The Manual

Liquidation preference

A term determining who gets paid first—and how much—when a company is sold. Investors with preferences receive their investment back before common shareholders (founders, employees) see anything. When a company exits below its last valuation, as Brex did, preferences determine whether late-stage investors recover capital while early employees might see their equity evaporate. It's the clause that separates "good outcome" from "good for some."

What we're watching

- Anthropic round close — The final investor lineup and terms will signal how institutional appetite for AI foundation models holds at these valuation levels.

- Fintech M&A pace — Whether the Capital One/Brex deal triggers additional consolidation among growth-stage fintechs seeking exits below peak valuations.

- IPO pipeline sequencing — Which mega-cap company files first (SpaceX, OpenAI, Anthropic, Databricks) will set the tone for the entire 2026 listing market.

Augment Markets Inc. is a technology company offering software and data services. Brokerage services are offered through Augment Capital LLC, an affiliated broker-dealer and member FINRA/SIPC. Investment advisory services are offered through Augment Advisors LLC, an SEC-registered investment adviser.

Important Disclosures: This material has been prepared for informational purposes only. None of the information provided represents a recommendation, an offer or the solicitation of an offer to buy or sell any security. The information provided does not constitute investment, legal, tax, or accounting advice. You should consult with qualified professionals before making any investment decisions. Investing in private securities involves substantial risk, including the potential loss of principal. Private securities are typically illiquid, have limited pricing transparency, and often require longer holding periods. These investments are available exclusively to qualified accredited investors and offer no guarantee of returns. An IPO or other liquidity event is not guaranteed. Additionally, past performance of private securities does not indicate or predict future results. Share price data are estimates only, based on proprietary data from Caplight and Augment Markets Inc. and its affiliates.

Paul leads editorial at Augment, building Pulse into the private markets' go-to intelligence source. He also develops editorial content strategies for startups and venture capital firms. Previously, he spent 15 years as a business and opinion journalist at The New York Times, Fortune, Fast Company, Reuters, and more. He believes transparency creates liquidity—and that someone should actually publish what private shares are trading for. He lives in Marin with his wife and two rescue dogs, and wishes he had more time to surf.

Learn more

FOR QUALIFIED INSTITUTIONAL AND ACCREDITED INVESTORS ONLY: Under federal securities laws, private market investments on this platform are available exclusively to Institutional and Accredited Investors. Verification of status required before investing. Private investments involve significant risks including illiquidity, potential loss of principal, and limited disclosure requirements. "Augment" refers to Augment Markets, Inc. and its affiliates. Augment Markets, Inc. is a technology company offering software and data services, not a bank or financial institution. Cash Accounts are provided by Modern Treasury Corp. financial institution partners and through Augment's technology. Augment does not act as a money services business, provide money transmission, or serve as a custodian of funds. Funds held in your Cash Account are not FDIC insured unless expressly disclosed. Full terms available in the Augment Cash Account Agreement.Brokerage services are offered through Augment Capital, LLC, an affiliated broker-dealer and member FINRA/SIPC. “Investment accounts” are not brokerage accounts and do not hold customer funds or securities. Investment advisory services are offered through Augment Advisors, LLC, an SEC-registered investment adviser. Registration with the SEC does not imply a certain level of skill or training. Augment and its affiliates do not provide legal or tax advice; consult your attorney or tax professional regarding your specific situation. For additional information, please refer to Augment Advisors, LLC’s Form ADV Part 2A (Firm Brochure) and FINRA BrokerCheck.