.jpeg)

Humanoid robotics is experiencing an AI-infrastructure-style capital surge — Neura Robotics raising ~€1B backed by Tether, Embo raising $100M+ for world models, and Arda raising $70M for manufacturing AI, all announced this week. Combined with Skild AI ($1.4B), Figure AI ($1B at $39B), and Apptronik ($935M at $5.3B) from recent months, investors have committed over $15 billion to humanoid and embodied AI startups since mid-2024. The question: is this the early innings of a trillion-dollar market, or the next overheated category? Let's Deep Dive and find out.

Deep Dive

If you've been watching private markets for the past 18 months, the pattern should look familiar.

A wave of capital sweeps into a technology category. Valuations triple in under a year. Strategic investors — Nvidia, Google, SoftBank, Amazon — race to stake positions. Founders with impressive research credentials raise nine-figure seed rounds before shipping a product. Everyone talks about trillion-dollar addressable markets.

In 2024-2025, that category was AI infrastructure — compute, chips, cloud. Now it's happening again. The category: humanoid robots and embodied AI.

Just this week: German startup Neura Robotics is raising approximately €1 billion backed by stablecoin issuer Tether, at a reported valuation of roughly €4 billion. Embo, a startup co-founded by former Google DeepMind research scientists, is in talks to raise a seed round of more than $100 million led by Andreessen Horowitz to build "world models" for robotics. And Arda, co-founded by former OpenAI chief research officer Bob McGrew, is reportedly raising $70 million at a $700 million valuation to automate manufacturing using AI.

None of these are isolated bets. They're data points in a capital deployment pattern that's accelerating faster than the underlying technology.

The Funding Map

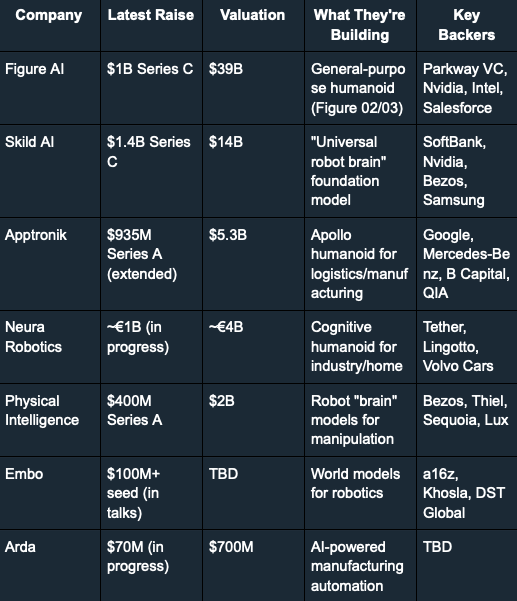

Here's what the robotics capital stack looks like heading into Q2 2026:

That's over $5 billion in funding from this table alone — and it represents only a slice of the broader robotics investment landscape. Crunchbase data shows robotics startups pulled in over $6 billion in the first half of 2025, and the pace has only increased since.

Why the capital is flowing now

Three converging forces are driving the surge, and they echo almost exactly what happened with AI infrastructure spending:

1. The "foundation model" thesis extends to physical AI

The same scaling-laws logic that made investors comfortable writing $10 billion checks for language models is now being applied to robotics. The argument: if you can train a single AI model to operate any robot — regardless of its physical form — you've built the "operating system" for the physical world. Skild AI's pitch is literally a "universal robot brain." Figure AI is building what it calls the Helix embodied intelligence platform. Google DeepMind's Gemini Robotics models are being deployed through partnerships with Apptronik.

This is the Byrne Hobart framing of structural advantages applied to atoms: whoever builds the general-purpose AI layer for robots captures platform economics in the physical world.

2. Strategic investors are treating it as a land grab

Look at the investor rosters: Nvidia shows up in Figure AI, Skild AI, and (through NVentures) multiple others. Google is backing Apptronik through both investment and its DeepMind partnership. SoftBank led Skild's round. Jeff Bezos has personal positions in at least two humanoid startups.

These aren't passive financial bets. They're strategic positioning plays by companies that expect to sell the compute, the cloud, and the AI models that robots will run on. Nvidia CEO Jensen Huang has described robotics as a "multitrillion-dollar opportunity" — and Nvidia's incentive is to make sure every robot runs on its chips, regardless of which startup builds the hardware.

3. The talent exodus from frontier AI labs

Embo's founders came from Google DeepMind. Arda's co-founder was OpenAI's chief research officer. Physical Intelligence was co-founded by researchers from Google Brain, Stanford, and UC Berkeley. The most accomplished AI researchers in the world are deciding that robotics — not language models — is where the next breakthrough happens.

This mirrors what happened in 2022-2023 when top researchers left Google and OpenAI to start AI infrastructure companies. When talent of this caliber moves, capital follows.

The skeptic's case

The parallels to AI infrastructure spending are instructive — but they cut both ways.

The deployment gap is real. Andreessen Horowitz published an extensive analysis in January acknowledging that while research progress in embodied AI has been remarkable, "almost none of it is deployed." There's a meaningful gap between a robot performing a task in a controlled lab demo and reliably executing that same task 10,000 times in a warehouse. Rodney Brooks, founder of iRobot, has been perhaps the most prominent skeptic, observing that "deployment at scale takes so much longer than anyone ever imagines."

The valuations are extraordinary. Figure AI at $39 billion has limited revenue from commercial deployments. Skild AI at $14 billion tripled its valuation in seven months. Apptronik's investors paid roughly 3x the initial Series A price for extension shares — a premium signal, but also an indication of how fast expectations are running ahead of traction.

Revenue remains minimal. Unlike the AI infrastructure boom, where companies like CoreWeave could point to real contracts with hyperscalers burning through tokens, most humanoid robotics companies are pre-revenue or generating revenue primarily from pilot programs and research partnerships. Anduril — which builds defense robots — is the exception, with revenue reportedly on track to hit $2 billion. But Anduril is selling to a customer (the U.S. military) with functionally unlimited demand and less price sensitivity than commercial buyers.

Manufacturing is hard. The history of hardware startups is littered with companies that could build a brilliant prototype but couldn't manufacture at scale. Figure AI plans to ship 100,000 humanoids over four years from its BotQ factory. Neura Robotics aims for 5 million robots by 2030. These are ambitious production targets for companies that have never manufactured at volume.

What this means for private market investors

If you're watching this category through the lens of secondary market activity, a few dynamics are worth flagging:

The investor base is unusual. Tether backing a German robotics company. Stablecoin profits funding humanoid robots. Qatar Investment Authority investing in Austin-based bipedal machines alongside John Deere. This isn't a traditional venture syndicate — it's a grab bag of strategic capital, sovereign wealth, and crypto profits looking for physical-world exposure. Unusual investor bases can mean unusual exit dynamics.

The IPO pipeline may be years away. Unlike AI companies like Anthropic and OpenAI that are generating billions in revenue and actively preparing for public offerings, most humanoid robotics companies are in an earlier stage of commercial development. This extends the timeline for liquidity events and means secondary markets may become important earlier in the lifecycle — particularly for employees at companies like Figure AI ($39B valuation) who may want to realize some value before a public offering that could be five or more years out.

The comparison set is limited. There are very few public companies that serve as direct comps for humanoid robotics startups. Tesla has Optimus but doesn't break out its financials. Intuitive Surgical is a robotics company but operates in a completely different market. This makes secondary pricing challenging — buyers and sellers have limited reference points for what these companies should be worth relative to their public peers.

The bottom line

Private markets are experiencing a capital deployment pattern in robotics that closely mirrors what happened in AI infrastructure 18 months ago: exponential valuation growth, research-talent-driven company formation, strategic investor land grabs, and ambitious production timelines that may or may not be achievable.

The optimistic read is that this is the early innings of the next computing platform — that humanoid robots will do for the physical world what AI models are doing for the digital one, and that the companies being funded today will be worth multiples of their current valuations within a decade.

The cautious read is that the technology is further from commercialization than the capital suggests, that valuations already reflect success scenarios, and that the gap between lab demos and factory-floor deployment may take longer to close than investors expect.

Both reads have evidence behind them. The capital flowing into this space isn't irrational — Nvidia, Google, and SoftBank don't write billion-dollar checks on a whim. But the lesson from every previous hardware investment cycle is that timing matters at least as much as thesis. Being right about the future of robotics and being early by five years can look a lot like being wrong.

Quick Takes

Anthropic nears $20B revenue run rate amid Pentagon feud — Anthropic's annualized revenue has reportedly surged past $19 billion, more than doubling since year-end 2025. The growth was driven by strong enterprise adoption of Claude Code. The milestone comes as the company faces a supply chain risk designation from the Pentagon over disputed terms of use for military applications.

Anduril raises $4B at $60B valuation — Thrive Capital and a16z co-led the round for Palmer Luckey's defense tech company, doubling its valuation in under a year. Lux Capital and Founders Fund also participated. The raise coincides with heightened U.S. military spending and the ongoing conflict with Iran.

SpaceX targets March confidential IPO filing — SpaceX is reportedly preparing to submit draft IPO paperwork to the SEC this month, keeping it on track for a potential June listing at a valuation that may exceed $1.75 trillion. Bank of America, Goldman Sachs, JPMorgan, and Morgan Stanley have reportedly been tapped for senior roles.

Fundrise Innovation Fund lists on NYSE as "VCX" — A publicly traded venture capital fund holding positions in SpaceX, Anthropic, OpenAI, Databricks, Anduril, and Ramp begins trading on or after March 9. The fund is designed to give non-accredited investors access to private tech companies — a notable milestone for the democratization of private market investing.

🎓 Manual

World Model

In robotics and AI, a world model is a neural network trained to simulate how the physical environment behaves — predicting what happens next given a robot's actions. Think of it as giving a robot an internal physics engine it can use to "imagine" the consequences of its movements before actually executing them. World models are considered a key ingredient in building robots that can generalize to new tasks and environments without requiring retraining for each specific scenario.

What We're Watching

- The Anthropic legal challenge — Whether and when Anthropic files suit against the Pentagon's supply chain risk designation. The outcome may reshape how the government interacts with AI companies on terms of use and deployment restrictions.

- SpaceX S-1 timing — A confidential filing this month would be the clearest signal yet that the largest IPO in history is on track for a summer listing.

- Robotics deployment milestones — Watch for Figure AI's BotQ factory production numbers and Apptronik's Google DeepMind deployment results. The gap between capital raised and commercial traction will determine whether current valuations are justified.

Augment Markets Inc. is a technology company offering software and data services. Brokerage services are offered through Augment Capital LLC, an affiliated broker-dealer and member FINRA/SIPC. Investment advisory services are offered through Augment Advisors LLC, an SEC-registered investment adviser.

Important Disclosures: This material has been prepared for informational purposes only. None of the information provided represents a recommendation, an offer or the solicitation of an offer to buy or sell any security. The information provided does not constitute investment, legal, tax, or accounting advice. You should consult with qualified professionals before making any investment decisions. Investing in private securities involves substantial risk, including the potential loss of principal. Private securities are typically illiquid, have limited pricing transparency, and often require longer holding periods. These investments are available exclusively to qualified accredited investors and offer no guarantee of returns. An IPO or other liquidity event is not guaranteed. Additionally, past performance of private securities does not indicate or predict future results. Share price data are estimates only, based on proprietary data from Caplight and Augment Markets Inc. and its affiliates.

Paul leads editorial at Augment, building Pulse into the private markets' go-to intelligence source. He also develops editorial content strategies for startups and venture capital firms. Previously, he spent 15 years as a business and opinion journalist at The New York Times, Fortune, Fast Company, Reuters, and more. He believes transparency creates liquidity—and that someone should actually publish what private shares are trading for. He lives in Marin with his wife and two rescue dogs, and wishes he had more time to surf.

Learn more

FOR QUALIFIED INSTITUTIONAL AND ACCREDITED INVESTORS ONLY: Under federal securities laws, private market investments on this platform are available exclusively to Institutional and Accredited Investors. Verification of status required before investing. Private investments involve significant risks including illiquidity, potential loss of principal, and limited disclosure requirements. "Augment" refers to Augment Markets, Inc. and its affiliates. Augment Markets, Inc. is a technology company offering software and data services, not a bank or financial institution. Cash Accounts are provided by Modern Treasury Corp. financial institution partners and through Augment's technology. Augment does not act as a money services business, provide money transmission, or serve as a custodian of funds. Funds held in your Cash Account are not FDIC insured unless expressly disclosed. Full terms available in the Augment Cash Account Agreement.Brokerage services are offered through Augment Capital, LLC, an affiliated broker-dealer and member FINRA/SIPC. “Investment accounts” are not brokerage accounts and do not hold customer funds or securities. Investment advisory services are offered through Augment Advisors, LLC, an SEC-registered investment adviser. Registration with the SEC does not imply a certain level of skill or training. Augment and its affiliates do not provide legal or tax advice; consult your attorney or tax professional regarding your specific situation. For additional information, please refer to Augment Advisors, LLC’s Form ADV Part 2A (Firm Brochure) and FINRA BrokerCheck.