The $285B wakeup call—and the $100B+ bet on what comes next

.jpeg)

The Market Stopped Treating AI Disruption as a Theoretical Risk.

On Monday and Tuesday, a selloff that traders are calling the "SaaSpocalypse" erased roughly $285 billion in market capitalization across software, legal technology, financial services, and asset management stocks. The trigger was remarkably small: Anthropic released eleven open-source plugins for Claude Cowork, its agentic AI assistant for non-technical professionals. The plugins included tools for contract review, NDA triage, compliance monitoring, and legal risk assessment.

The reaction was anything but small. Thomson Reuters fell 16%—its largest single-day decline on record. LegalZoom dropped 20%. Goldman Sachs' US software basket fell 6%, its steepest slide since the April 2025 tariff shock. Blue Owl Capital, Ares, Apollo, KKR, TPG, and Blackstone all declined sharply. Indian IT services firms Infosys, TCS, and Wipro fell roughly 6% in sympathy. The Nasdaq-100 dropped 2.4% intraday before closing down 1.6%.

Here's what makes this genuinely interesting for private market watchers: Anthropic didn't launch a product. It published prompt instructions in a GitHub repo. The plugins are open-source. The code is freely available for anyone to read, copy, or modify.

The market reacted to "Anthropic" plus "legal" without fully parsing what was actually shipped. As one analyst noted, prompts aren't the moat—execution, trust, integration, and compliance are. But the selloff revealed something important about how capital markets are pricing AI risk: not gradually, and not rationally. When a foundation-model company packages what looks like a professional workflow tool, the market reprices the incumbents first and asks questions later.

For private market investors, the implication is directional. Only 71% of S&P 500 software companies beat revenue estimates this earnings season, compared to 85% for the broader tech sector. Software is growing slower and earning less than hardware, cloud, and platform providers. The SaaSpocalypse may have been an overreaction on any given name—but as a category signal, it's hard to ignore.

The NFX Thesis: AI Games Are Coming

While the software selloff dominated headlines, venture firm NFX published a piece this week that deserves attention from anyone tracking where the next wave of AI-native companies will emerge.

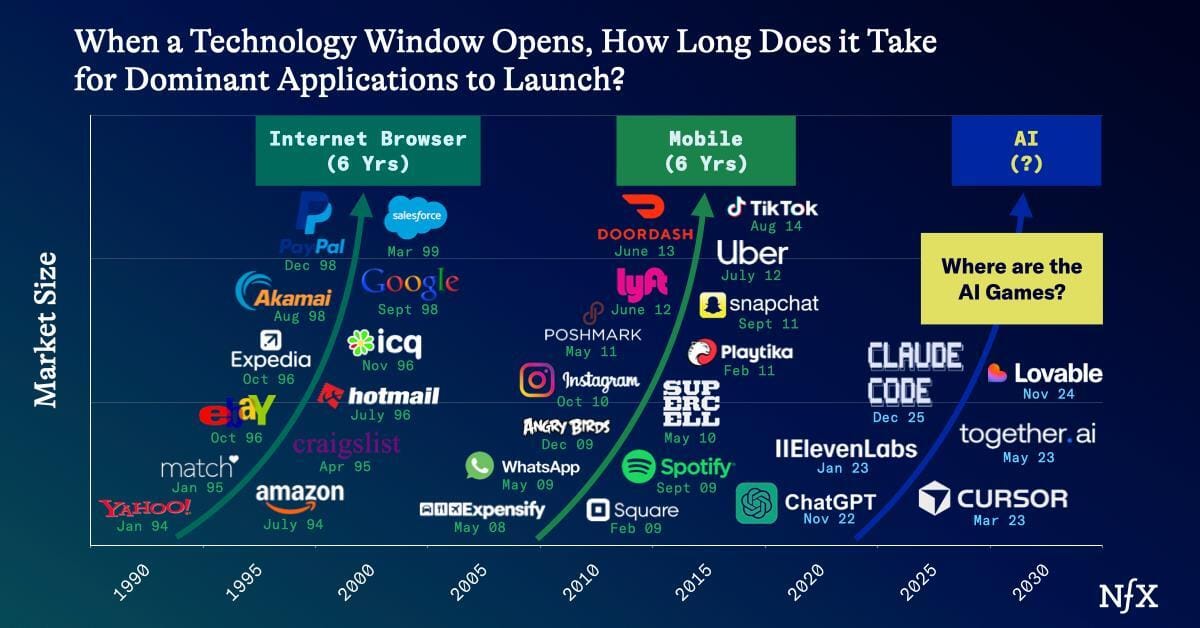

The thesis: AI gaming's technology window has just opened—but the massive breakout hasn't happened yet, and that's exactly what makes it interesting.

NFX partner James Currier draws a historical parallel: When the internet's technology window opened in July 1993, games didn't arrive for nearly a decade. Runescape launched in 2001. Second Life in 2003. World of Warcraft in 2004. Roblox in 2006. Minecraft in 2009. The browser alone wasn't sufficient—games needed bandwidth, video processing, and memory to catch up.

Mobile was different. Because foundational technologies arrived simultaneously with the app store, Angry Birds, Supercell, and Playtika all launched within three years.

The question for AI: which pattern does it follow?

Currier argues the technology window has just cracked open—inference speed, cost, quality, memory management, and generative media (image, video, voice, music) are all improving rapidly but haven't yet converged into a seamless creative platform. He also identifies a founder mindset gap: most game developers are still thinking in traditional formats rather than imagining what AI-native entertainment looks like. Think Roblox and Minecraft more than Call of Duty. Think experiences where LLM hallucinations become features, not bugs. Think slow-motion gameplay that works even with generation latency.

The commercial stakes are substantial. Gaming is already larger than the film and music industries combined. NFX is hosting an invitation-only AI Games Summit in San Francisco on March 8—the day before GDC—sponsored by Silicon Valley Bank and Latitude Games, the studio behind AI Dungeon, arguably the closest thing to an AI-native breakout so far.

Why this matters for private markets: Early-stage AI gaming companies represent a category where the technology window analysis suggests patient capital has asymmetric upside. The infrastructure is still arriving, most founders haven't adjusted their mental models, and the market is enormous. When the convergence happens—and NFX's historical analysis suggests it's a matter of when, not if—the companies building now will have a meaningful head start.

Funding Pulse

Over $2 billion in new funding landed this week across AI infrastructure, voice, DevOps, chips, and robotics. Here's what's notable:

Cerebras: $1B at $23B Valuation

The AI chip maker nearly tripled its valuation from $8.1 billion just five months ago—its second billion-dollar round since September. Tiger Global led, with AMD, Benchmark, Coatue, and 1789 Capital among investors. The round is Cerebras' first since it withdrew its U.S. IPO filing in October, underscoring a broader trend of companies staying private longer with abundant capital available outside public markets. Meanwhile, Reuters reported that OpenAI has been seeking alternatives to Nvidia for inference chips, including Cerebras, AMD, and Groq. Nvidia reportedly approached Cerebras about a potential acquisition; the company declined and struck a commercial deal with OpenAI instead. Cerebras is known for its wafer-scale engine chips, designed to accelerate both training and inference of large AI models. Reuters

ElevenLabs: $500M (Series D)

The voice and audio AI company raised $500 million, reportedly tripling its valuation. The round underscores continued investor appetite for the middleware layer between foundation models and end-user applications. ElevenLabs is expanding into multimodal AI agents—moving beyond voice synthesis into broader agentic capabilities. The company's text-to-speech and voice cloning technology has become a standard tool across media, gaming, and enterprise communications. Sifted

Positron: $230M at $1B+ Valuation (Series B)

The Reno-based inference chip startup reached unicorn status in a round co-led by Arena Private Wealth, Jump Trading, and Unless, with strategic investment from Qatar Investment Authority and Arm Holdings. What's notable here isn't just the valuation—it's the customer-to-investor conversion. Jump Trading started as a Positron customer, tested the company's Atlas system, saw roughly 3x lower end-to-end latency versus comparable H100-based configurations on inference workloads, and then co-led the round. The company has spent only $38 million to date and is already shipping hardware manufactured in Arizona. Startup Researcher

Resolve AI: $125M at $1B Valuation (Series A)

An autonomous site reliability engineering platform that hit unicorn status 16 months after emerging from stealth. Led by Lightspeed Venture Partners with Greylock Partners, the round brings total funding to over $150 million. Resolve's product autonomously handles incident diagnosis, rollback decisions, capacity adjustments, and guided code changes. One client reported a 72% reduction in time to investigate critical incidents. Its customer list includes Coinbase, DoorDash, MongoDB, and Salesforce. Founders Spiros Xanthos and Mayank Agrawal are observability veterans who co-created OpenTelemetry (the open-source telemetry standard) and previously sold companies to Splunk and VMware. The pitch: as AI agents generate more code faster, the bottleneck shifts from writing software to running it reliably. SiliconAngle

Bedrock Robotics: $270M (Series B)

The autonomous construction vehicle company raised $270 million co-led by CapitalG (Google's growth fund) and Valor Atreides AI Fund. Bedrock deploys autonomous fleets for earthmoving and site preparation—among the most labor-intensive and dangerous segments of commercial construction. The round signals growing investor conviction that physical AI's first commercial applications may be in industrial settings rather than consumer robotics. The Robot Report

📊 Data Point of the Day

2,500

That's the approximate number of lines of code—prompt instructions, really—that Anthropic published as open-source GitHub plugins for Claude Cowork on January 30. The market's response: $285 billion in erased market capitalization across SaaS, legal tech, and financial services. The ratio of lines of code to dollars destroyed may be unprecedented.

🎓 Manual

Technology Window

The period during which foundational technologies converge to make a new category of products viable. Coined in the context of platform shifts, it describes why some categories (social networks, mobile apps) emerge rapidly while others (internet gaming, VR) take years. The width of the window depends on how many underlying technologies need to mature simultaneously. NFX's analysis suggests AI gaming's technology window has just opened—but the full convergence of inference speed, generative media quality, and developer tooling may take 2-4 more years.

What We're Watching

- Cerebras staying private — The company withdrew its IPO filing in October, then raised $1B at $23B. With OpenAI reportedly seeking Nvidia alternatives and Nvidia's own acquisition approach rebuffed, Cerebras is positioning itself as an independent challenger with no near-term pressure to go public. Watch whether the OpenAI commercial deal translates to meaningful revenue diversification.

- SaaSpocalypse aftershocks — Earnings season continues. Watch for software companies explicitly addressing AI competitive risk in guidance calls. The market is now pricing this in; companies that don't have a credible AI strategy may face further pressure.

- Inference chip category formation — Positron, Cerebras, Groq ($6.9B), and Etched ($5B) are collectively raising billions to challenge Nvidia's dominant market share in AI compute. Whether this capital translates to commercial traction in 2026-2027 will determine if "Nvidia alternative" becomes a real investment category or remains aspirational.

Augment Markets Inc. is a technology company offering software and data services. Brokerage services are offered through Augment Capital LLC, an affiliated broker-dealer and member FINRA/SIPC. Investment advisory services are offered through Augment Advisors LLC, an SEC-registered investment adviser.

Important Disclosures: This material has been prepared for informational purposes only. None of the information provided represents a recommendation, an offer or the solicitation of an offer to buy or sell any security. The information provided does not constitute investment, legal, tax, or accounting advice. You should consult with qualified professionals before making any investment decisions. Investing in private securities involves substantial risk, including the potential loss of principal. Private securities are typically illiquid, have limited pricing transparency, and often require longer holding periods. These investments are available exclusively to qualified accredited investors and offer no guarantee of returns. An IPO or other liquidity event is not guaranteed. Additionally, past performance of private securities does not indicate or predict future results. Share price data are estimates only, based on proprietary data from Caplight and Augment Markets Inc. and its affiliates.

Paul leads editorial at Augment, building Pulse into the private markets' go-to intelligence source. He also develops editorial content strategies for startups and venture capital firms. Previously, he spent 15 years as a business and opinion journalist at The New York Times, Fortune, Fast Company, Reuters, and more. He believes transparency creates liquidity—and that someone should actually publish what private shares are trading for. He lives in Marin with his wife and two rescue dogs, and wishes he had more time to surf.

Learn more

FOR QUALIFIED INSTITUTIONAL AND ACCREDITED INVESTORS ONLY: Under federal securities laws, private market investments on this platform are available exclusively to Institutional and Accredited Investors. Verification of status required before investing. Private investments involve significant risks including illiquidity, potential loss of principal, and limited disclosure requirements. "Augment" refers to Augment Markets, Inc. and its affiliates. Augment Markets, Inc. is a technology company offering software and data services, not a bank or financial institution. Cash Accounts are provided by Modern Treasury Corp. financial institution partners and through Augment's technology. Augment does not act as a money services business, provide money transmission, or serve as a custodian of funds. Funds held in your Cash Account are not FDIC insured unless expressly disclosed. Full terms available in the Augment Cash Account Agreement.Brokerage services are offered through Augment Capital, LLC, an affiliated broker-dealer and member FINRA/SIPC. “Investment accounts” are not brokerage accounts and do not hold customer funds or securities. Investment advisory services are offered through Augment Advisors, LLC, an SEC-registered investment adviser. Registration with the SEC does not imply a certain level of skill or training. Augment and its affiliates do not provide legal or tax advice; consult your attorney or tax professional regarding your specific situation. For additional information, please refer to Augment Advisors, LLC’s Form ADV Part 2A (Firm Brochure) and FINRA BrokerCheck.