.jpeg)

PitchBook's 2025 Annual US VC Secondary Market Watch

PitchBook released its annual deep dive into venture secondaries this week, and it should be required reading for anyone participating in — or thinking about participating in — the private markets. Here's what stood out, what it means, and what the report doesn't say.

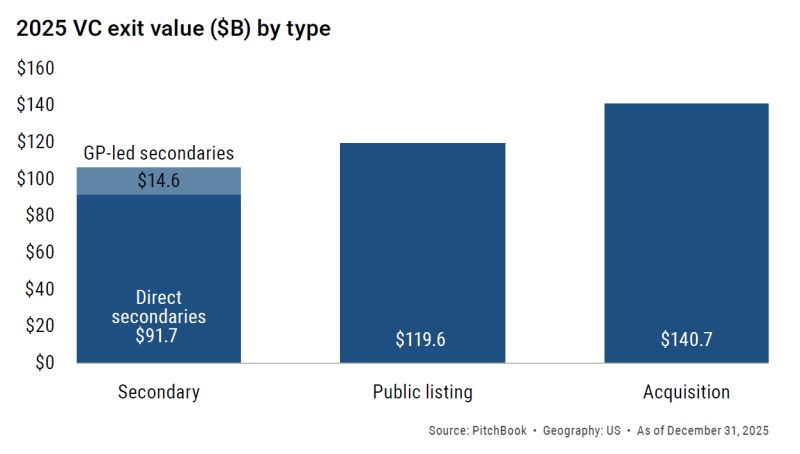

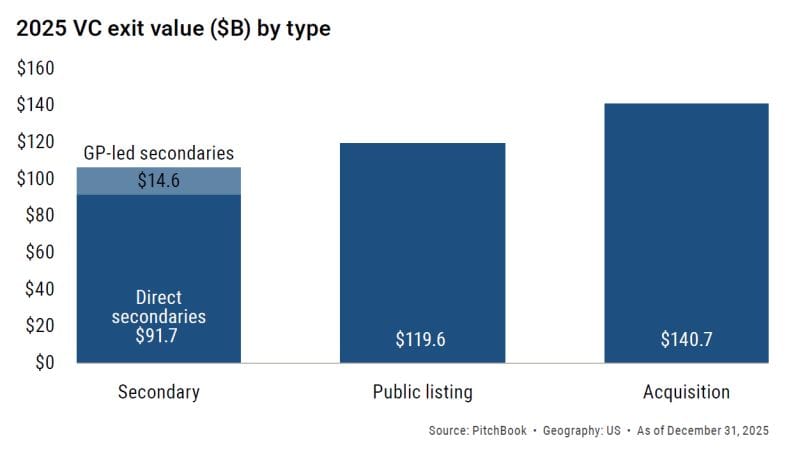

The big number: $106.3 billion. That's PitchBook's estimate for total U.S. venture secondary transaction value in 2025, combining $91.7 billion in direct secondaries with $14.6 billion in GP-led transactions. To put that in perspective, public listings generated $119.6 billion and acquisitions generated $140.7 billion in venture exit value over the same period. Secondaries are no longer a niche liquidity tool. They're approaching parity with the two traditional exit routes.

But the range tells the real story. PitchBook's estimate for direct secondaries alone spans $62.5 billion to $120.9 billion — a range wider than the entire global soap market, as Fortune’s Allie Garfinkle helpfully pointed out this week. That $58 billion gap exists because the secondary market remains structurally opaque. There are limited disclosure requirements, many deals happen through small brokerages or direct negotiations, and the biggest names distort everything. The range isn't a flaw in PitchBook's methodology. It's a feature of the market itself.

The concentration problem

The report's most striking data point, in our view: on Hiive, the top 20 startups accounted for 86.4% of secondary trading value in Q4 2025. The top five alone — names like SpaceX and OpenAI — represented 55.6%.

That kind of concentration means the market is approaching a significant transition. If SpaceX, OpenAI, and Anthropic all go public in 2026 (as current reporting suggests they're planning to), a massive share of secondary volume vanishes overnight.

PitchBook argues this reshaping is healthy, not destructive — and the data backs them up. More IPOs mean better pricing benchmarks, tighter bid-ask spreads, and more investor confidence. On Caplight, 70 companies saw their first secondary trade in 2025, totaling $492 million. The market is starting to broaden. But for now, secondaries remain a top-heavy business. SpaceX was the most actively traded name on Augment in Q4 2025, accounting for 12.5% of total platform activity. OpenAI's $6.6 billion tender offer in October alone made up 6.2% of annual secondary transaction value.

The question for 2026 is whether the market can redistribute liquidity beyond this small group of elite names — or whether the post-IPO vacuum creates a temporary contraction before the next wave of companies fills the gap.

Wall Street is all in

One of the report's clearest signals: every major financial institution is now racing to build or buy secondary market capabilities.

The list from the past few months alone is remarkable (and yes we’ve told you about some of these before, but not in this context): Goldman Sachs acquired Industry Ventures. Morgan Stanley acquired EquityZen. Charles Schwab acquired Forge Global. Nasdaq Private Market partnered with G Squared for priority access to tender offers. J.P. Morgan built a dedicated private capital team within its investment bank. Piper Sandler launched private markets trading after hiring senior talent from Forge.

These are billion-dollar acquisitions and strategic hires/tie-ups that signal where institutional capital thinks the market is heading. As PitchBook puts it: secondaries are now central to how capital is raised, allocated, and returned.

Tender offers are becoming standard practice

Stripe's announcement yesterday — a tender offer at a $159 billion valuation, up 49% from $106.7 billion just five months ago — is a perfect illustration of one of the report's key themes: company-led liquidity programs are becoming the norm, not the exception.

PitchBook cataloged 14 notable tender offers in 2025. SpaceX ran a $2.6 billion tender in December. OpenAI's $6.6 billion tender in October was the largest of the year. Ramp, Rippling, Whatnot, Notion, Vercel, ElevenLabs, Plaid — the list reads like a who's who of late-stage venture.

There's a straightforward logic here. Nearly half of today's unicorns (48.5%, per PitchBook) had their first VC round in 2016 or earlier. That means early employees and investors have been waiting a decade or more for liquidity. Regular tender offers solve the talent retention problem — employees don't need to leave for a public company to get paid — while giving startups more control over their cap tables than third-party secondary transactions provide.

Stripe is the clearest example of this model working at scale. Profitable, processing $1.9 trillion in payment volume, growing 34% year-over-year — and still no IPO plans. When co-founder John Collison says the company is in "no rush" to go public, it's because the private liquidity infrastructure now works well enough that going public is a choice, not a requirement.

The dry powder story

The report shows venture secondary dry powder reached $11.8 billion as of mid-2025, up 2.8x from 2022. That growth is significant, but the context matters more: $11.8 billion still represents just 3.9% of the capital held by primary VC funds.

In other words, for every $100 that venture capital allocates to initial investments, less than $4 is earmarked for buying existing shares on the secondary market. The opportunity set is enormous relative to the capital currently targeting it.

New entrants are responding. Pinegrove Opportunity Partners closed a $2.2 billion debut venture secondary fund. Insight Partners hired from Industry Ventures to build its own secondaries strategy. StepStone's most recent fund hit $3.3 billion. The buyer base is expanding — but it's still early innings.

The SPV warning

Not everything in the report is optimistic. PitchBook flags growing concerns around special purpose vehicles — the pooled investment structures that allow smaller investors to access pre-IPO shares. The typical secondary SPV on Sydecar in 2025 raised $930,000 from nine investors in just 16 days, charging 2% management fees and 10% carry.

As demand surged, so did complexity — and bad actors. Multilayered SPVs made it harder to trace actual share ownership. FINRA's 2026 oversight report flagged misrepresentation and disclosure failures. Linqto filed for bankruptcy. A Sestante Capital manager was indicted for fraud.

The implication: SPVs will persist, but startups are tightening the rules around who can form them and who can invest. Buyers need to scrutinize structures carefully — understanding information rights, fee layers, and whether the SPV can actually verify ownership of the underlying shares. Access is concentrating among established, trusted operators.

What the report says about 2026

PitchBook's outlook can be summarized in one line: secondaries are moving from proving relevance to becoming embedded infrastructure.

The structural case is clear. Companies are staying private longer. Traditional exits remain constrained. Institutional capital is flooding in. AI, crypto, defense, and aerospace — sectors aligned with U.S. policy priorities — are capturing outsized secondary volume. AI startups see higher valuation step-ups at every funding stage compared to non-AI peers, which creates more paper gains and more incentive for employees and early investors to seek partial liquidity.

The open question is concentration. Can the market function efficiently when 86% of trading volume is in just 20 companies? What happens when several of those companies go public? PitchBook's data suggests the broadening has already started — but 2026 will be the real test.

📊 Data Point of the Day

3.9%

That's venture secondary dry powder as a share of primary VC capital. For a market that traded over $100 billion last year, the dedicated buyer capital is still remarkably small relative to the opportunity — suggesting significant room for institutional expansion.

Source: PitchBook, as of June 2025

🎓 Manual

Forward Contract

A secondary market transaction where a buyer agrees to purchase shares at a set price, but the actual transfer is contingent on a future event — typically the company's right of first refusal (ROFR) clearance or board approval. Forwards have grown as a share of secondary deal structures as more startups tighten transfer restrictions. For buyers, they offer price certainty in a volatile market. The risk: if the company blocks the transfer, the deal dies. Understanding whether a transaction is structured as a direct transfer, an SPV, or a forward contract is increasingly important as issuers assert more control over who ends up on their cap table.

Augment Markets Inc. is a technology company offering software and data services. Brokerage services are offered through Augment Capital LLC, an affiliated broker-dealer and member FINRA/SIPC. Investment advisory services are offered through Augment Advisors LLC, an SEC-registered investment adviser.

Important Disclosures: This material has been prepared for informational purposes only. None of the information provided represents a recommendation, an offer or the solicitation of an offer to buy or sell any security. The information provided does not constitute investment, legal, tax, or accounting advice. You should consult with qualified professionals before making any investment decisions. Investing in private securities involves substantial risk, including the potential loss of principal. Private securities are typically illiquid, have limited pricing transparency, and often require longer holding periods. These investments are available exclusively to qualified accredited investors and offer no guarantee of returns. An IPO or other liquidity event is not guaranteed. Additionally, past performance of private securities does not indicate or predict future results. Share price data are estimates only, based on proprietary data from Caplight and Augment Markets Inc. and its affiliates.

Paul leads editorial at Augment, building Pulse into the private markets' go-to intelligence source. He also develops editorial content strategies for startups and venture capital firms. Previously, he spent 15 years as a business and opinion journalist at The New York Times, Fortune, Fast Company, Reuters, and more. He believes transparency creates liquidity—and that someone should actually publish what private shares are trading for. He lives in Marin with his wife and two rescue dogs, and wishes he had more time to surf.

Learn more

FOR QUALIFIED INSTITUTIONAL AND ACCREDITED INVESTORS ONLY: Under federal securities laws, private market investments on this platform are available exclusively to Institutional and Accredited Investors. Verification of status required before investing. Private investments involve significant risks including illiquidity, potential loss of principal, and limited disclosure requirements. "Augment" refers to Augment Markets, Inc. and its affiliates. Augment Markets, Inc. is a technology company offering software and data services, not a bank or financial institution. Cash Accounts are provided by Modern Treasury Corp. financial institution partners and through Augment's technology. Augment does not act as a money services business, provide money transmission, or serve as a custodian of funds. Funds held in your Cash Account are not FDIC insured unless expressly disclosed. Full terms available in the Augment Cash Account Agreement.Brokerage services are offered through Augment Capital, LLC, an affiliated broker-dealer and member FINRA/SIPC. “Investment accounts” are not brokerage accounts and do not hold customer funds or securities. Investment advisory services are offered through Augment Advisors, LLC, an SEC-registered investment adviser. Registration with the SEC does not imply a certain level of skill or training. Augment and its affiliates do not provide legal or tax advice; consult your attorney or tax professional regarding your specific situation. For additional information, please refer to Augment Advisors, LLC’s Form ADV Part 2A (Firm Brochure) and FINRA BrokerCheck.