From $68B to $11B: Figma's lesson for private investors

.jpeg)

Welcome back to the Thursday Deep Dive.

Why We're Covering a Public Company

Pulse covers private markets. So why are we dedicating a deep dive to Figma, which went public seven months ago?

Because Figma's post-IPO trajectory offers something rare: a live case study in how the market reprices "AI-era" software companies when optimism meets reality.

Many of the highest-valued private companies today—from design tools to developer platforms to vertical SaaS—carry valuations predicated on similar narratives: category leadership, strong retention metrics, and AI upside. Figma checked all those boxes. It still does. And yet the stock is down 84% from its peak.

For investors evaluating private opportunities on Augment's marketplace, Figma's experience raises questions worth asking before you buy:

- How much of this valuation is AI narrative vs. AI revenue?

- What happens if the company stumbles on AI execution?

- Could AI actually disrupt the core product rather than enhance it?

- Can a startup outspend incumbents on AI infrastructure?

Figma isn't a warning that all software investments are doomed. It's a reminder that the gap between private market valuations and public market reality can close violently—and that execution risk in AI cuts both ways.

The Setup: A Historic IPO

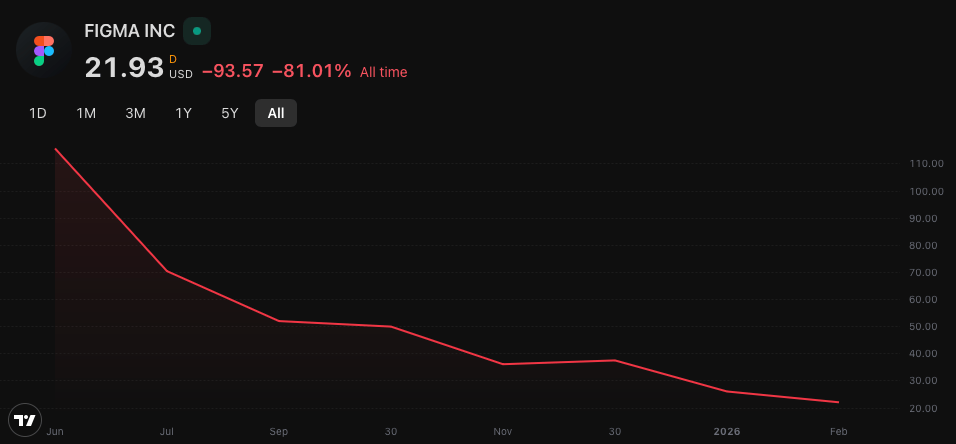

Figma went public on July 31, 2025 priced at $33 per share. The stock opened at $85, closed its first day at $115.50, and peaked at $142.92 within 48 hours—a 250% first-day pop that marked the largest IPO gain for a deal raising over $1 billion in more than three decades.

At its peak, Figma commanded a market cap of approximately $68 billion. Today it trades around $21—below its IPO price—with a market cap of roughly $11 billion.

The fundamentals didn't collapse. Revenue grew 38% year-over-year in Q3. Net dollar retention among customers spending $10K+ annually sits at 131%. The company crossed $1 billion in ARR. By most SaaS metrics, this is still a strong business.

So what happened?

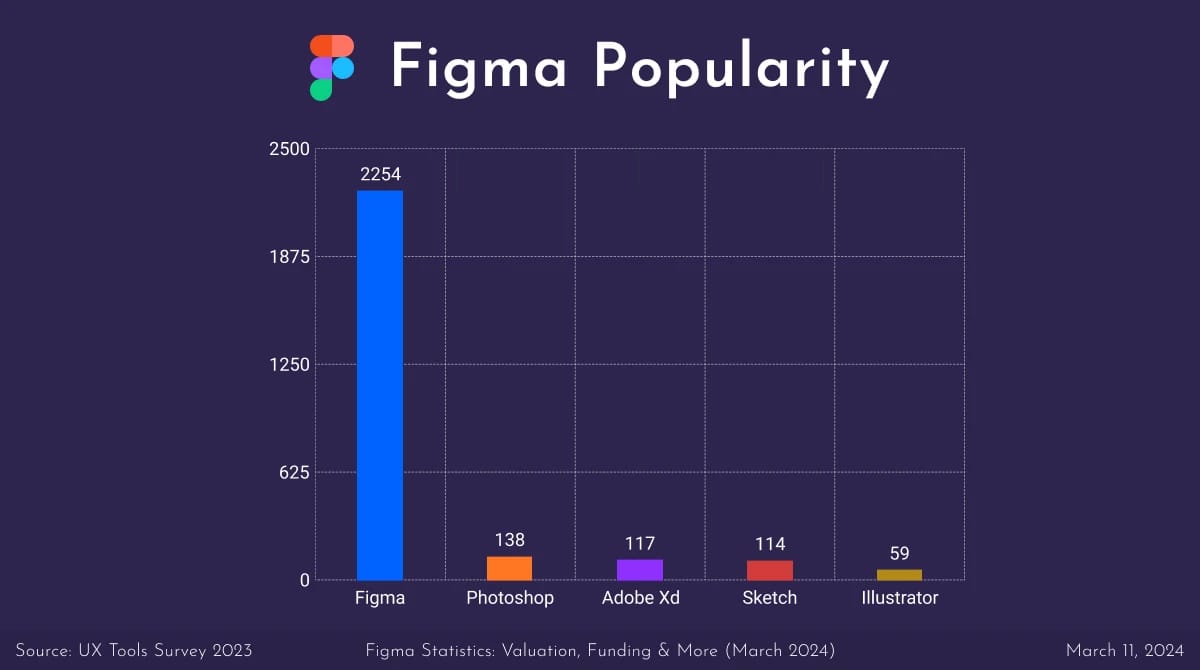

Lesson 1: AI Market Share Doesn't Follow Product Market Share

Figma dominates UI/UX design—estimates range from 41% to 80-90% market share depending on how you define the category. That dominance among designers hasn't translated to AI.

Figma Make, the company's generative AI design tool launched alongside the IPO in July 2025, holds approximately 2% of the AI design tool market. Adobe Firefly commands 29%—more than Midjourney, Canva AI, or DALL-E.

The difference? Distribution. Firefly is embedded directly into Photoshop, Illustrator, and the broader Creative Cloud suite. When 32.5 million Creative Cloud subscribers open their tools, Firefly is already there. Microsoft Designer ships as part of Microsoft 365's 400+ million paid seats.

Figma Make, by contrast, requires users to discover and adopt a new capability within an existing workflow. The company is building a consumption-based AI business from scratch while competing against incumbents who can bundle AI as table stakes.

The private market lesson: Category leadership in the core product doesn't guarantee AI leadership. When evaluating private companies, ask: Who has the distribution advantage for AI features? Can the startup afford to give AI away while building adoption, or must it monetize immediately?

Lesson 2: The MCP Server Tells the Real Story

Sometimes the most revealing signal isn't in an earnings report—it's in how developers react to a company's tools.

Figma launched an official MCP (Model Context Protocol) server to let AI coding agents access design context. The response from the developer community was telling. One widely-shared post titled "A Better Figma MCP" called the official implementation "pretty underwhelming at best" and "so useless that it's clear that it only exists as a means for Figma to control the narrative."

The core criticism: Figma's official MCP is deliberately one-way. You can pull context about your design, but you can't manipulate the design itself. The developer community responded by building alternatives—there are now 38+ community Figma MCP servers that offer capabilities the official server doesn't.

Why would Figma limit its own tool? The post answers directly: "if you can use AI to generate designs, well you know what comes next."

The private market lesson: Watch how companies handle AI integration into their core products. Are they enabling the ecosystem or protecting it? Defensive AI strategies may preserve short-term revenue but signal long-term vulnerability. The most confident platforms lean into openness.

Lesson 3: AI Can Compress the Market, Not Expand It

The deeper challenge facing Figma is structural: What if AI coding tools eliminate the design step entirely?

Figma dominates a specific workflow—designer creates mockup, developer translates to code. AI tools like Cursor, Claude Code, and Replit are compressing that workflow. An engineer can describe an interface in plain language and receive working components in return. For the millions of Figma users who were never designers to begin with—product managers, engineers, executives—that shortcut matters.

As one recent analysis put it: "Design becomes output, not process."

Figma sees this clearly. At Config 2025, the company announced AI-native products (Figma Make with Claude, Figma Sites, Figma Buzz) designed to position it as the orchestration layer for AI-assisted workflows. In October 2025, it acquired Israeli AI startup Weavy for more than $200 million to bolster that bet.

The private market lesson: When evaluating any software company, ask the hardest question: Does AI expand this company's market, or compress it? Category leaders can become category casualties if AI reshapes workflows rather than augmenting them. The most dangerous assumption is that AI helps incumbents by default.

Lesson 4: The Balance Sheet Fight

Here's the uncomfortable math. Adobe can afford to spend billions on AI over the next four years. Figma cannot.

Adobe Firefly has already generated $400 million in direct revenue and contributed 11% of Creative Cloud's new ARR. The company can afford to embed AI everywhere and monetize through its existing credit system and enterprise contracts. Microsoft doesn't even need to directly monetize Designer—it's a feature that drives 365 retention.

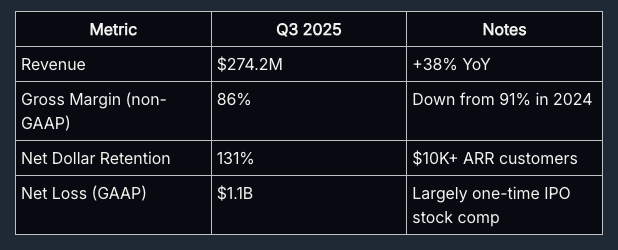

Figma's gross margins have fallen from 91% to 83-86% over the past 18 months as AI infrastructure spending climbed. The company is investing heavily in AI capabilities that aren't yet contributing materially to revenue, while competing against companies that can afford to give those same capabilities away.

Q3 2025 results showed the tension:

The private market lesson: AI execution requires capital. Lots of it. When evaluating private companies at premium valuations, ask: Can this company win an AI spending war against entrenched incumbents? Or is the AI narrative priced in without the balance sheet to back it up?

Lesson 5: The Multiple Compression Math

Here's the arithmetic that keeps late-stage private investors up at night:

Figma priced its IPO at $33 per share, implying roughly a $12 billion valuation on ~$750 million in trailing revenue—approximately 16x revenue. At its peak ($143), the market briefly valued it at 90x+ revenue. Today, at $21, it trades around 10-11x forward revenue.

That's a reasonable multiple for a 38%-growth SaaS company. But it's a long way from the 30-50x multiples some private software companies still command in secondary markets.

The private market lesson: Strong fundamentals don't guarantee strong multiples. The market now demands proof that AI investments translate to revenue, not just product announcements. When evaluating private companies at premium valuations, stress-test what multiple compression looks like—because the exit environment has changed.

What to Watch: February 18 Earnings

Figma reports Q4 and full-year 2025 results after market close on February 18.

Key questions relevant to private market investors:

- AI monetization timeline: When does AI consumption become material? Figma has indicated 2026 expectations.

- Gross margin trajectory: Will AI infrastructure costs continue pressuring the premium SaaS profile?

- Competitive positioning: How is management framing the threat from AI coding tools and Adobe's AI distribution advantage?

The answers will shape not just Figma's multiple, but market expectations for the entire design and developer tools category—including private companies you might be evaluating today.

The Bottom Line

Figma's 84% drawdown reflects four overlapping concerns: typical post-IPO volatility, AI execution that trails the competition, structural questions about whether AI compresses design workflows, and a balance sheet fight it may not be able to win.

The company's fundamentals remain solid. But investors who bought at peak valuations—public or private—are learning that "strong retention + AI optionality" doesn't guarantee multiple expansion. Execution matters. Competitive dynamics matter. And the gap between private market optimism and public market scrutiny can close faster than anyone expects.

Figma isn't a cautionary tale about a bad company. It's a real-time lesson in how the market stress-tests good companies priced for perfection in an AI environment that rewards execution, not narrative. In twelve months, Figma could be a turnaround story or a permanent warning. Either way, private market valuations haven't fully absorbed what public markets are now demanding: AI revenue, not AI optionality. The next time you see a private company trading at 30x revenue with "AI upside" in the pitch deck, ask yourself what's already priced in—and what happens if the narrative doesn't deliver.

Augment Markets Inc. is a technology company offering software and data services. Brokerage services are offered through Augment Capital LLC, an affiliated broker-dealer and member FINRA/SIPC. Investment advisory services are offered through Augment Advisors LLC, an SEC-registered investment adviser.

Important Disclosures: This material has been prepared for informational purposes only. None of the information provided represents a recommendation, an offer or the solicitation of an offer to buy or sell any security. The information provided does not constitute investment, legal, tax, or accounting advice. You should consult with qualified professionals before making any investment decisions. Investing in private securities involves substantial risk, including the potential loss of principal. Private securities are typically illiquid, have limited pricing transparency, and often require longer holding periods. These investments are available exclusively to qualified accredited investors and offer no guarantee of returns. An IPO or other liquidity event is not guaranteed. Additionally, past performance of private securities does not indicate or predict future results. Share price data are estimates only, based on proprietary data from Caplight and Augment Markets Inc. and its affiliates.

Paul leads editorial at Augment, building Pulse into the private markets' go-to intelligence source. He also develops editorial content strategies for startups and venture capital firms. Previously, he spent 15 years as a business and opinion journalist at The New York Times, Fortune, Fast Company, Reuters, and more. He believes transparency creates liquidity—and that someone should actually publish what private shares are trading for. He lives in Marin with his wife and two rescue dogs, and wishes he had more time to surf.

Learn more

FOR QUALIFIED INSTITUTIONAL AND ACCREDITED INVESTORS ONLY: Under federal securities laws, private market investments on this platform are available exclusively to Institutional and Accredited Investors. Verification of status required before investing. Private investments involve significant risks including illiquidity, potential loss of principal, and limited disclosure requirements. "Augment" refers to Augment Markets, Inc. and its affiliates. Augment Markets, Inc. is a technology company offering software and data services, not a bank or financial institution. Cash Accounts are provided by Modern Treasury Corp. financial institution partners and through Augment's technology. Augment does not act as a money services business, provide money transmission, or serve as a custodian of funds. Funds held in your Cash Account are not FDIC insured unless expressly disclosed. Full terms available in the Augment Cash Account Agreement.Brokerage services are offered through Augment Capital, LLC, an affiliated broker-dealer and member FINRA/SIPC. “Investment accounts” are not brokerage accounts and do not hold customer funds or securities. Investment advisory services are offered through Augment Advisors, LLC, an SEC-registered investment adviser. Registration with the SEC does not imply a certain level of skill or training. Augment and its affiliates do not provide legal or tax advice; consult your attorney or tax professional regarding your specific situation. For additional information, please refer to Augment Advisors, LLC’s Form ADV Part 2A (Firm Brochure) and FINRA BrokerCheck.