Bezos raises $12B; Citi tokenizes private shares; SpaceX IPOs

.jpeg)

SpaceX priced the largest IPO on record Thursday night and began trading on Nasdaq — Thursday's deep dive, updated with the pricing, covers what its exit means for the private tape. Other highlights: Jeff Bezos' Prometheus closed a $12 billion Series B at a reported $41 billion valuation, Citigroup said it will offer tokenized shares of private companies to wealthy clients, and KKR launched a $10 billion AI-infrastructure financier. Capital moved at IPO scale all week. Most of it without a ticker.

🤖 The Big Story: A Series B the size of an IPO

Jeff Bezos announced Prometheus’ capital raise during a week of significant IPO activity, which highlights the continued ability of select private companies to raise capital at very large scale. The industrial-AI company Bezos co-leads with Vik Bajaj, announced a $12 billion Series B at a reported $41 billion valuation Thursday — on the heels of a $6.2 billion Series A. (Axios · CNBC)

Look at the investor list. JPMorgan, BlackRock, Goldman Sachs, DST Global, Arch Venture Partners. That reads less like a venture syndicate than an underwriting group — the same institutions that would have built the book if a company at this scale had gone public to raise it. Instead they're on the cap table, at Series B, of a company building AI tools for engineering and manufacturing physical products that has reportedly raised more than $18 billion across two rounds.

One possible market-structure takeaway is that, for a small number of highly sought-after private issuers, private capital markets may provide access to financing at a scale that historically would have been associated with public offerings. Whether that remains durable will depend on market conditions, issuer fundamentals, investor demand, and regulatory consideration. SpaceX's listing and Prometheus' round landing in the same news cycle is the whole 2026 capital-formation picture in one day: the public market is back open for the largest names, and it is also, increasingly, optional.

Reported private-company financials and secondary-market indications may be unaudited, incomplete, non-standard, or based on limited transaction activity. They should not be relied upon as fair value, executable pricing, or a basis for any investment decision.

🏦 Second Story: Citi builds a rail for private shares

Citigroup is rolling out a blockchain-based platform for wealthy and institutional clients to trade tokenized shares of private companies, the Wall Street Journal reported Thursday. (WSJ · The Block)

The mechanics matter more than the crypto framing. Citi is partnering with SDX, the digital-asset arm of the SIX Swiss Exchange, and will act as custodian and tokenization agent — issuing tokenized depositary receipts that represent interests in private-company shares, held through regulated institutions. The platform starts with non-US investors; US access would depend on regulatory conditions. Citi says it is in discussions with some of the largest private companies about participating, and argues the structure could offer more transparency than the special-purpose vehicles often used to access pre-IPO names.

That last point is the one to sit with. Much of the access to top private names today runs through layered SPVs — structures that can make fees, terms, transfer restrictions, and underlying exposure more difficult for investors to evaluate. A global bank standing up custody-grade infrastructure for the same exposure is a statement about where this asset class is headed: out of the workaround era, toward standing rails. Whether tokenization is the rail that wins is a separate question — but the fact that the bid for one now comes from a balance sheet like Citi's says the demand is no longer in dispute.

⚡ Third Story: KKR launches a $10B AI-infrastructure financier

KKR launched Helix Digital Infrastructure on Wednesday — a new company with more than $10 billion in committed capital from KKR, the Kuwait Investment Authority, and Nvidia, with Vistra as preferred power provider and former AWS CEO Adam Selipsky running it. (Business Wire) The pitch: data centers, power, and connectivity financed and delivered under one platform, at hyperscaler speed.

The same day brought the counterpoint. Crusoe said it has "paused" a planned Wyoming data center; Bloomberg reported the project failed to win customers — including Google — amid concerns about costs and timetable. (Bloomberg) The buildout capital is enormous, but it is not indiscriminate: projects with anchored demand and integrated power are getting platform-scale backing, while projects without committed customers are stalling. For private-market observers, the financing layer of the AI buildout is consolidating into fewer, larger vehicles — and the gap between funded and stranded projects appears to be widening.

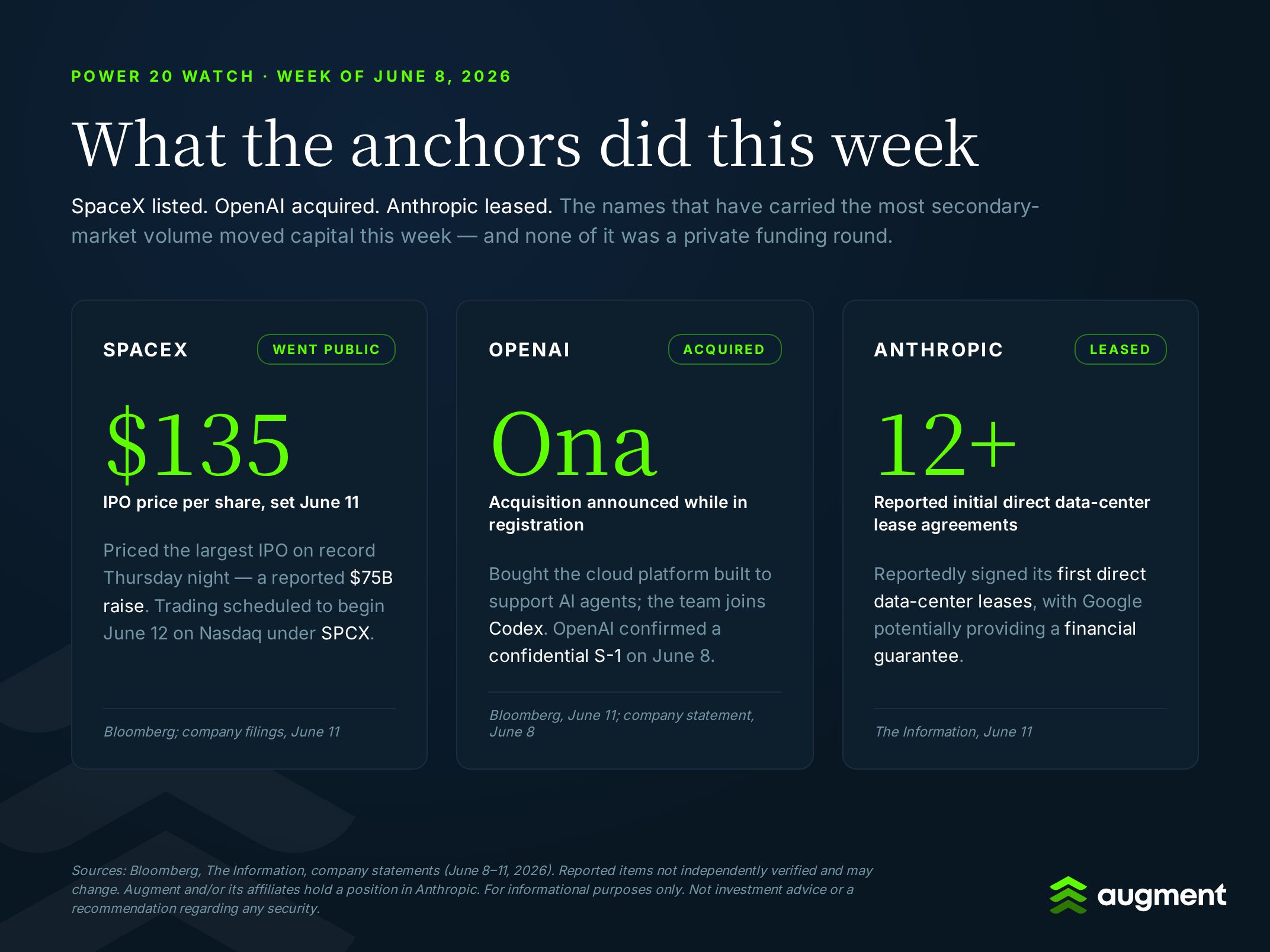

👑 Power 20 Watch: The anchor lifts today

"Power 20" refers to Augment's internal ranking of selected private-market activity based on platform trading activity and reported secondary-market interest. It may not represent the broader private market and should not be treated as a valuation benchmark.

SpaceX priced Thursday night, and Thursday's deep dive — updated with the numbers — covers the pricing and what the exit may mean for the private tape, so we won't relitigate it here. (Bloomberg pegs the post-pricing market value at $1.77 trillion. (Bloomberg))

What's new since that piece published is the shape of the book. BlackRock placed an order for at least $5 billion of shares, per the Journal (WSJ), and retail investors are expected to be allocated at least 20% of available shares (Bloomberg) — the retail-access question the deep dive raised, now with reported numbers attached. Not everyone is convinced: the New York Times reports some investors question the valuation, citing a $4.3 billion loss on $4.7 billion in revenue in Q1. (NYT) Trading is scheduled to begin this morning on Nasdaq under SPCX.

The other new development is what the remaining anchors did this week — and it wasn't equity. OpenAI acquired Ona, a cloud platform for AI agents, folding the team into Codex. (Bloomberg) Anthropic reportedly signed more than a dozen initial agreements for direct data-center leases — a first for the company — with Google potentially providing a financial guarantee, per The Information. (The Information) Leases, guarantees, acquisitions, infrastructure vehicles: the largest private names are increasingly financing their buildouts through structures other than primary equity rounds, which changes where the obligations sit on the way to any eventual listing.

Augment and/or its affiliates hold a position in Anthropic. References to Anthropic and other named issuers are for illustrative market-commentary purposes only and are not recommendations or investment opinions.

Reported private-company financials and secondary-market indications may be unaudited, incomplete, non-standard, or based on limited transaction activity. They should not be relied upon as fair value, executable pricing, or a basis for any investment decision.

💨 Quick Takes

- OpenAI acquires Ona — the cloud-services startup supports AI agents; its team joins OpenAI's Codex effort. The acquisition is notable because it occurred while the company is reportedly in the registration process.

- Apollo screens every software investment for AI risk — the firm built a framework sorting software companies into 12–14 sectors ranked by susceptibility to AI disruption. When a major private-equity buyer formalizes "AI threat" as underwriting criteria, that framework may start showing up in how late-stage software gets priced.

- Meta completes its split from Manus — Meta has stopped data sharing after China ordered the buyout unwound; Manus is reportedly exploring options including raising roughly $1 billion to fund a buyback. A reminder that cross-border deal risk now runs in both directions.

- Anthropic and OpenAI keep expanding in London — CNBC reports the city has emerged as the key AI talent hub outside the US over the past year of lab expansions.

💰The Funding Lineup

The following financing rounds are included for market context only and are not recommendations or valuation opinions.

- Genspark — $100M Series B extension at $2.6B post-money (June 11). The agentic-workplace startup's valuation is up 63% in roughly three months; it has raised more than $645 million to date. The interval between marks keeps compressing for agentic software.

- Theker — $85M led by CRV (June 11). The Barcelona company builds AI-powered robots for industrial environments, with Samsung and LVMH among participants. Strategics buying into European robotics is a quieter version of the industrial-AI thesis Prometheus just raised $12 billion on.

- Digital Asset — $355M, including $100M from a16z crypto (June 11). Digital Asset builds Canton Network, a public blockchain with privacy features already used by Wall Street institutions. Tokenization rails are getting funded the same week Citi committed to building on them — the infrastructure and the distribution are arriving together.

- PhoenixAI — $80M Series B led by Sky9 (June 11). Formerly CelerData, the company is building what it calls an agentic-AI-ready analytical database — the data layer underneath the agent wave.

- Coram AI — $35M Series B (June 11). The startup layers AI onto organizations' existing security cameras to find incidents, bringing total funding to $66 million. Physical-world AI applied to installed hardware, not new fleets.

📈 Data Point of the Day

2.5 billion gallons

That's how much water Amazon says its data centers used in 2025 — about 0.12 liters per kilowatt-hour, with water use at sites it owns and operates down 2% from 2024. (WSJ) The week's headlines were about who finances the AI buildout; this number is about what the buildout consumes. As hyperscalers begin disclosing water the way they disclose power, physical-resource metrics are becoming part of how data-center projects get evaluated — and, as Crusoe's paused Wyoming project suggests, part of why some don't get built.

Reported private-company financials and secondary-market indications may be unaudited, incomplete, non-standard, or based on limited transaction activity. They should not be relied upon as fair value, executable pricing, or a basis for any investment decision.

🎓 Manual

Tokenized Depositary Receipt

A digital token recorded on a blockchain that represents ownership of an interest in a traditional security — in this case, private-company shares — held by a regulated custodian. The token isn't the share itself; it's a claim on the share, the way an ADR represents foreign stock held by a depositary bank. In private markets, the structure may allow approved investors to hold and transfer private-company exposure through standard custody accounts, though the underlying shares remain subject to the same transfer restrictions, issuer consent requirements, and illiquidity as any private security.

👀 What We're Watching

- SpaceX's first public prints. Trading began this morning under SPCX after Thursday's $135 pricing. (Bloomberg) The first sessions establish a public reference point for one of the most actively followed private names. How the early float behaves, given how much stock remains locked up, is one structural question worth tracking into subsequent trading days.

- OpenAI's path through registration. The company confirmed a confidential S-1 on June 8, with a listing reportedly possible as early as September. (Fortune) Because the filing is confidential, terms, timing, and structure remain unknown — and this week's Ona acquisition shows the company isn't pausing M&A while in registration.

- How the labs finance compute. Anthropic's reported first direct data-center leases — with a potential Google financial guarantee — would mark a shift from buying compute through cloud partners to carrying lease obligations directly. (The Information) Additional lease disclosures, if they emerge, may clarify how much of the buildout sits on lab balance sheets versus partners'.

- The step-up cadence. Genspark's 63% markup arrived roughly three months after its last round. (Axios) Whether compressed re-rate intervals persist across agentic software — or whether this week's cluster proves to be a local peak — is one thing to monitor as the IPO window absorbs the largest names.

Augment Markets Inc. is a technology company offering software and data services. Brokerage services are offered through Augment Capital LLC, an affiliated broker-dealer and member FINRA/SIPC. Investment advisory services are offered through Augment Advisors LLC, an SEC-registered investment adviser.

Important Disclosures: This material has been prepared for informational purposes only. None of the information provided represents a recommendation, an offer or the solicitation of an offer to buy or sell any security. The information provided does not constitute investment, legal, tax, or accounting advice. You should consult with qualified professionals before making any investment decisions. Investing in private securities involves substantial risk, including the potential loss of principal. Private securities are typically illiquid, have limited pricing transparency, and often require longer holding periods. These investments are available exclusively to qualified accredited investors and offer no guarantee of returns. An IPO or other liquidity event is not guaranteed. Additionally, past performance of private securities does not indicate or predict future results. Share price data are estimates only, based on proprietary data from Caplight and Augment Markets Inc. and its affiliates.

Paul leads editorial at Augment, building Pulse into the private markets' go-to intelligence source. He also develops editorial content strategies for startups and venture capital firms. Previously, he spent 15 years as a business and opinion journalist at The New York Times, Fortune, Fast Company, Reuters, and more. He believes transparency creates liquidity—and that someone should actually publish what private shares are trading for. He lives in Marin with his wife and two rescue dogs, and wishes he had more time to surf.

Learn more

FOR QUALIFIED INSTITUTIONAL AND ACCREDITED INVESTORS ONLY: Under federal securities laws, private market investments on this platform are available exclusively to Institutional and Accredited Investors. Verification of status required before investing. Private investments involve significant risks including illiquidity, potential loss of principal, and limited disclosure requirements. "Augment" refers to Augment Markets, Inc. and its affiliates. Augment Markets, Inc. is a technology company offering software and data services, not a bank or financial institution. Cash Accounts are provided by Modern Treasury Corp. financial institution partners and through Augment's technology. Augment does not act as a money services business, provide money transmission, or serve as a custodian of funds. Funds held in your Cash Account are not FDIC insured unless expressly disclosed. Full terms available in the Augment Cash Account Agreement.Brokerage services are offered through Augment Capital, LLC, an affiliated broker-dealer and member FINRA/SIPC. “Investment accounts” are not brokerage accounts and do not hold customer funds or securities. Investment advisory services are offered through Augment Advisors, LLC, an SEC-registered investment adviser. Registration with the SEC does not imply a certain level of skill or training. Augment and its affiliates do not provide legal or tax advice; consult your attorney or tax professional regarding your specific situation. For additional information, please refer to Augment Advisors, LLC’s Form ADV Part 2A (Firm Brochure) and FINRA BrokerCheck.