.jpeg)

OpenAI is reportedly leaning toward waiting until 2027 to list, with advisers pointing to recent tech-stock and SpaceX volatility — a timing question that keeps the most-wanted name in private hands longer. Capital kept moving toward "physical AI" and world models, with General Intuition's $320 million round and onsemi's $7 billion bid for Synaptics landing the same day. Underneath all of it, the memory layer tightened: Micron printed a record gross margin and Apple raised hardware prices, the AI buildout showing up on a consumer price tag. And SpaceX, the first Power 20 name with a public tape, gave back most of its post-IPO gains.

The Big Story: OpenAI's IPO clock, and the gap between $730 billion and $1 trillion

OpenAI is leaning toward holding its IPO until 2027, according to New York Times reporting cited by Bloomberg and the NYT itself. The reported reason is timing: bankers advising the company cautioned that recent volatility in tech stocks — and in SpaceX's shares after its record debut — could cool retail enthusiasm for an offering. Advisers reportedly framed it as a choice between waiting for the market to settle and the financials to mature, or accepting a lower valuation to move sooner. Sam Altman has reportedly held firm on a $1 trillion target.

That target is the part worth sitting with. OpenAI's last private round reportedly valued the company between $730 billion and $852 billion. The $1 trillion figure is an aspiration, not a mark — and the distance between the two is exactly the kind of gap the private market is built to argue about between funding events.

For secondary holders, a delay changes the math in a specific way. Tuesday's edition made the structural point through ByteDance: when a company can fund itself privately and run its own liquidity, the IPO becomes optional. OpenAI's situation is different in kind — this is a reported scheduling decision, not a decision to stay private indefinitely — but the effect on the secondary is similar in the near term. A name that doesn't list in 2026 is a name whose shares keep changing hands privately, on marks that move with each reported round rather than a daily close. The longer a company remains private, the more investors may look to private financing rounds, tender offers, and secondary indications for valuation reference points. Those reference points can be useful, but they may be limited, non-transparent, transaction-specific, and materially different from executable pricing or fair value.

One observation worth tracking: whether OpenAI's gap closes by the company growing into the number, or by the market re-rating the number down to the company. Those are very different outcomes for anyone holding the name today, and the reporting suggests the people closest to the deal don't yet agree on which one is coming.

Reported private-company financials and secondary-market indications may be unaudited, incomplete, non-standard, or based on limited transaction activity. They should not be relied upon as fair value, executable pricing, or a basis for any investment decision.

Second Story: The money is rotating toward AI that acts, not AI that writes

Two deals landed on the same day that, read together, point in one direction. General Intuition raised a $320 million Series A at a $2.3 billion valuation, led by Khosla Ventures with Eric Schmidt's Hillspire and Jeff Bezos participating. The company trains "large action" models on action-labeled gameplay clips and builds world models — systems meant to act across space and time rather than generate text. Hours earlier, onsemi agreed to buy Synaptics in a $7 billion all-stock dealexplicitly framed around "physical AI" — the sensors and silicon that let machines perceive and act in the world.

The through-line is a rotation. As the foundation-model layer commoditizes, capital is moving up the stack toward embodiment: robotics, spatial reasoning, world simulation, the hardware underneath it. Patronus AI's $50 million roundthe same week — building simulated environments to stress-test AI agents — sits in the same theme.

For private-market readers, the signal isn't any single valuation. It's where the marquee names are writing checks. When Bezos and Schmidt anchor a Series A in a category, that category tends to attract the next tier of capital, which is how a theme becomes a cohort and a cohort becomes a wave of secondary supply two years out. The physical-AI names are early enough that most have no secondary float to speak of. That's worth noting now, because the cohort that's getting funded this quarter is the cohort whose shares desks will be sourcing in 2027 and 2028.

Reported private-company financials and secondary-market indications may be unaudited, incomplete, non-standard, or based on limited transaction activity. They should not be relied upon as fair value, executable pricing, or a basis for any investment decision.

Third Story: The AI buildout showed up on a price tag this week

The least glamorous layer of the AI story had its loudest week in a while. Micron reported a record adjusted gross margin— reportedly around 84.9%, with its entire 2026 high-bandwidth-memory supply already sold out under fixed-price contracts. Days later, Apple raised prices on Macs and iPads, citing component costs it said it had never seen rise this fast. The cause is the same in both cases: data-center demand is pulling memory supply away from everything else, and DRAM contract prices have been climbing at the steepest pace TrendForce tracks.

The private-market read is the mirror image of Tuesday's credit story. The AI buildout is being financed as infrastructure — long-dated contracts, structured debt — and now it's being priced like a commodity squeeze too. Memory has become a gating input, and the companies that locked in supply have an edge that doesn't show up in a model-quality benchmark. For anyone marking the AI infrastructure cluster, supply access is quietly becoming as material as compute access was a year ago.

Reported private-company financials and secondary-market indications may be unaudited, incomplete, non-standard, or based on limited transaction activity. They should not be relied upon as fair value, executable pricing, or a basis for any investment decision.

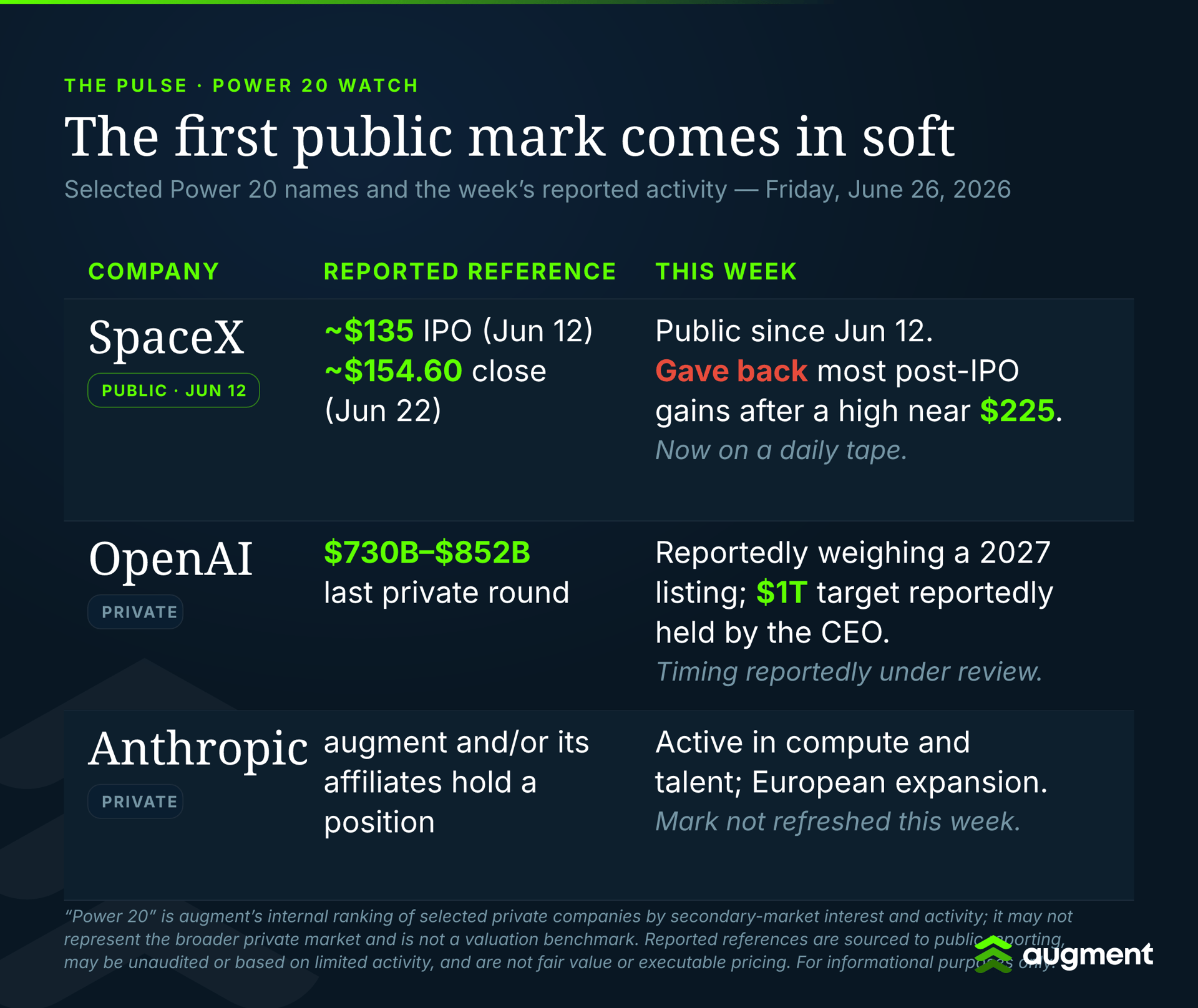

Power 20 Watch: The first public mark comes in soft

"Power 20" refers to Augment's internal ranking of selected high-profile private companies by secondary-market interest and activity. It may not represent the broader private market and should not be treated as a valuation benchmark.

For a year, the Power 20 has been a list of names without a public price. SpaceX changed that on June 12, and the three weeks since are an early lesson in what happens when a private mark meets a daily close. After listing at $135 and reaching an intraday high near $225.64 on June 16, the stock sold off hard, closing around $154.60 on June 22 — still above its IPO price, but having surrendered most of its post-debut gains, as Yahoo Finance and Al Jazeera both noted.

That matters beyond SpaceX, because it's the first public comp the rest of the Power 20 will be measured against. When the only listed name in the cohort trades back toward its debut, the reported reluctance from OpenAI's advisers to rush a 2026 listing reads less like caution and more like a read of the same tape.

The structural question for the cohort: if the first public Power 20 name settles below its opening enthusiasm, does that pull the band on private marks for the names still waiting — or do desks treat one volatile debut as company-specific rather than a read on the group? Additional public listings from the cohort, if they occur, may provide context.

Reported private-company financials and secondary-market indications may be unaudited, incomplete, non-standard, or based on limited transaction activity. They should not be relied upon as fair value, executable pricing, or a basis for any investment decision.

💨 Quick Takes

- The White House asked OpenAI to stagger its next model release — Sam Altman reportedly told staff the U.S. government asked OpenAI to roll out GPT-5.6 gradually, approving access "customer by customer" over security concerns. A reminder that for frontier labs, regulatory posture is becoming a product-roadmap input, not just a compliance footnote.

- The U.S. put $250 million into a chip startup — The Commerce Department awarded CHIPS funds to I-Pulse, the silicon-carbide and pulsed-power venture co-founded by mining billionaire Robert Friedland. Government as a direct capital allocator in frontier hardware is becoming a recurring line item, not an exception.

- Kraken is in talks to take 15% of Aave — at a reported $385 million valuation, investing 35,000 ETH for 250,000 AAVE tokens. An exchange buying a strategic stake in a DeFi protocol is its own kind of private-market transaction, just settled in tokens rather than SPV units.

- Anthropic accused Alibaba of illicitly extracting model capabilities — the kind of IP dispute that lands differently when the companies involved are among the most valuable private and public names in AI. (Augment and/or its affiliates hold a position in Anthropic.)

💰The Funding Lineup

The following financing rounds are included for market context only and are not recommendations or valuation opinions.

- Nura Bio — $73.8M Series B (June 22) — The Bay Area biotech raised from The Column Group, Euclidean Capital, Samsara BioCapital, and Sanofi Ventures to fund a Phase 1b/2a study of an oral SARM1 inhibitor for ALS. A reminder that the deepest scientific risk in the venture market still sits outside AI — and still clears at nine figures when the data warrants.

- Patronus AI — $50M Series B (June 25) — Led by Greenfield, bringing total funding to $70 million. Patronus builds simulated environments to evaluate AI agents — infrastructure for the world-model wave, sold to the labs building it.

- xCures — $46M Series B (June 24) — Led by Innovius Capital at a reported $127 million post-money. The company uses AI to turn fragmented medical records into structured clinical data — healthcare AI's least glamorous, most durable use case.

- Nebulock — $25M Series A (June 25) — Led by FirstMark. The startup helps security teams proactively hunt threats across their stack, a sign that "agentic" security is now a fundable Series A category rather than a feature.

- Sail — $80M seed and Series A (June 25) — Emerged from stealth at a reported $450 million valuation, led by Kleiner Perkins. Sail's software optimizes how AI models run on existing chips — a direct play on the same compute-and-memory scarcity driving this week's Micron print.

- Netris — $15M Series A (June 25) — From a16z. Netris automates network configuration so neoclouds can bring data centers online faster — picks-and-shovels for the buildout, one layer below the GPUs everyone talks about.

📈 Data Point of the Day

84.9%

That's the record adjusted gross margin Micron reportedly posted in its June-quarter earnings — a number that, if it holds up against the company's filings, would top Nvidia's and Meta's, with its entire 2026 high-bandwidth-memory supply already sold out under fixed-price contracts (Tech Times). For the AI-infrastructure cluster, it's the cleanest read yet on where pricing power sits in the buildout: not at the model layer, where competition is fierce, but at the memory layer, where supply is scarce and contracts are locked.

🎓 Manual

Tender Offer

A tender offer in the private-company context is a company-organized opportunity for existing shareholders — usually employees and early investors — to sell some of their shares at a set price, often to the company itself or to incoming investors. It's the structured, issuer-blessed alternative to a one-off secondary sale, and it's how many late-stage companies provide liquidity without going public. As more names reportedly weigh longer timelines before listing, the tender offer is one of the mechanisms that may carry the liquidity load a delayed IPO would otherwise have provided.

👀 What We're Watching

- Whether OpenAI grows into $1 trillion or the number comes to it.The reported gap between OpenAI's last round ($730–852 billion) and its $1 trillion target is the single most-watched figure in private markets right now. Which way it closes — financials maturing or valuation re-rating — is worth tracking. (Bloomberg)

- Memory as the buildout's binding constraint. With Micron's HBM sold out and the cost now reaching consumer hardware, supply access — not just compute — may become a gating factor in AI-infrastructure economics. (Tech Times)

- Whether physical AI is a theme or a cohort. General Intuition's marquee backers and onsemi's $7 billion bet landed the same day. If the next tier of capital follows, this becomes the secondary supply of 2027–2028. (TechCrunch)

- Government as a frontier-hardware investor. The I-Pulse award puts federal capital directly into a private chip venture. Whether more frontier hardware gets funded through programs like CHIPS, alongside or instead of pure venture, is worth monitoring. (Bloomberg)

Augment Markets Inc. is a technology company offering software and data services. Brokerage services are offered through Augment Capital LLC, an affiliated broker-dealer and member FINRA/SIPC. Investment advisory services are offered through Augment Advisors LLC, an SEC-registered investment adviser.

Important Disclosures: This material has been prepared for informational purposes only. None of the information provided represents a recommendation, an offer or the solicitation of an offer to buy or sell any security. The information provided does not constitute investment, legal, tax, or accounting advice. You should consult with qualified professionals before making any investment decisions. Investing in private securities involves substantial risk, including the potential loss of principal. Private securities are typically illiquid, have limited pricing transparency, and often require longer holding periods. These investments are available exclusively to qualified accredited investors and offer no guarantee of returns. An IPO or other liquidity event is not guaranteed. Additionally, past performance of private securities does not indicate or predict future results. Share price data are estimates only, based on proprietary data from Caplight and Augment Markets Inc. and its affiliates.

Paul leads editorial at Augment, building Pulse into the private markets' go-to intelligence source. He also develops editorial content strategies for startups and venture capital firms. Previously, he spent 15 years as a business and opinion journalist at The New York Times, Fortune, Fast Company, Reuters, and more. He believes transparency creates liquidity—and that someone should actually publish what private shares are trading for. He lives in Marin with his wife and two rescue dogs, and wishes he had more time to surf.

Learn more

FOR QUALIFIED INSTITUTIONAL AND ACCREDITED INVESTORS ONLY: Under federal securities laws, private market investments on this platform are available exclusively to Institutional and Accredited Investors. Verification of status required before investing. Private investments involve significant risks including illiquidity, potential loss of principal, and limited disclosure requirements. "Augment" refers to Augment Markets, Inc. and its affiliates. Augment Markets, Inc. is a technology company offering software and data services, not a bank or financial institution. Cash Accounts are provided by Modern Treasury Corp. financial institution partners and through Augment's technology. Augment does not act as a money services business, provide money transmission, or serve as a custodian of funds. Funds held in your Cash Account are not FDIC insured unless expressly disclosed. Full terms available in the Augment Cash Account Agreement.Brokerage services are offered through Augment Capital, LLC, an affiliated broker-dealer and member FINRA/SIPC. “Investment accounts” are not brokerage accounts and do not hold customer funds or securities. Investment advisory services are offered through Augment Advisors, LLC, an SEC-registered investment adviser. Registration with the SEC does not imply a certain level of skill or training. Augment and its affiliates do not provide legal or tax advice; consult your attorney or tax professional regarding your specific situation. For additional information, please refer to Augment Advisors, LLC’s Form ADV Part 2A (Firm Brochure) and FINRA BrokerCheck.