.jpeg)

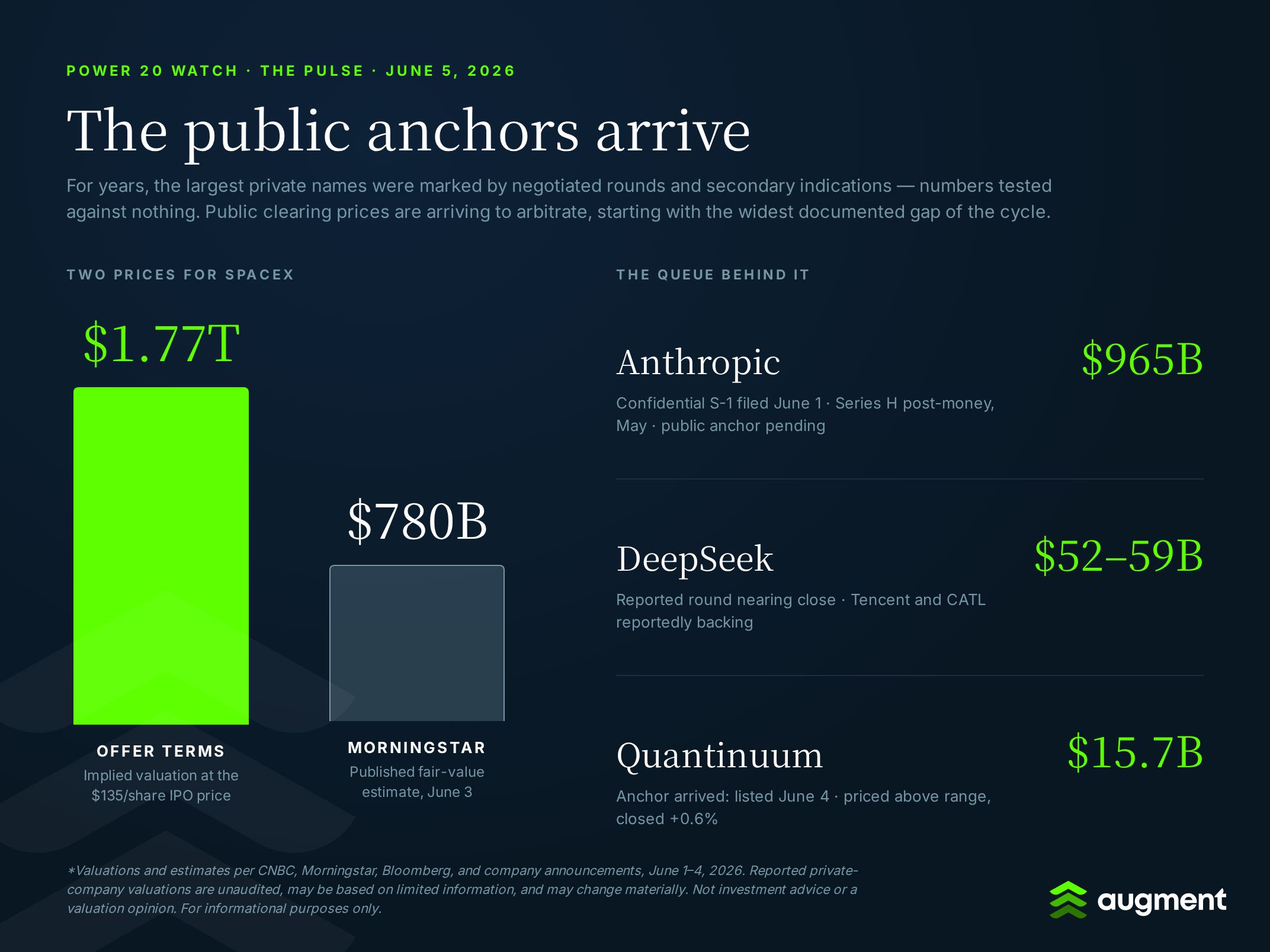

SpaceX set its IPO price at $135 a share — a fixed price, not a range — implying a $1.77 trillion valuation, and Morningstar answered with a published fair-value estimate of $780 billion. Washington, meanwhile, has reportedly held preliminary talks about the federal government taking equity stakes in AI companies, an idea Sam Altman has pitched directly to the President. And Quantinuum delivered the new IPO pipeline's first finished data point: priced above range, closed roughly where it priced.

🚀 The Big Story: SpaceX set its price. Morningstar published a different one.

On Wednesday, SpaceX set the price for its offering at $135 per share — a single fixed price rather than the conventional range — implying a roughly $1.77 trillion valuation once the IPO is complete, per CNBC. The company plans to sell about 555.6 million shares to raise roughly $75 billion, all of it primary — no existing holders are selling into the deal. Elon Musk would retain more than 82% voting control. The roadshow opens the week of June 8, with Nasdaq trading under the ticker SPCX possibly as soon as June 12. At $75 billion, the raise would be the largest on record, roughly triple Saudi Aramco's $25.6 billion in 2019.

Then came the second number. Morningstar initiated coverage with a fair-value estimate of $780 billion — less than half the offer valuation, per CNBC. The firm's discounted-cash-flow work values launch and Starlink at roughly $611 billion and assigns about $170 billion to probability-weighted AI scenarios, including a 43% probability that the orbital data center ambitions are shelved. At the offer valuation, SpaceX would trade at roughly 94 times its reported 2025 revenue of $18.67 billion, Fortune notes.

For private-market readers, the structure matters as much as the spread. An all-primary offering means existing holders — employees, early investors, secondary buyers who entered over the past year — get their liquidity later, through lock-up expirations, not at the listing. And the $1.77 trillion-versus-$780 billion gap is the first time a mega-cap private mark has met a published public dissent days before a clearing price arrives to arbitrate. The spread itself is the information; the tape will publish its answer within weeks.

Reported private-company financials and secondary-market indications may be unaudited, incomplete, non-standard, or based on limited transaction activity. They should not be relied upon as fair value, executable pricing, or a basis for any investment decision.

Sources: CNBC — SpaceX targets $135 IPO price · CNBC — Morningstar's $780B estimate · Fortune — the 94x revenue math · Globe and Mail — the fixed-price structure

Washington floats joining the AI cap table

Senior US officials have held preliminary talks with AI companies about the federal government acquiring shares in their firms, NOTUS reported Thursday. Sam Altman reportedly first pitched the concept directly to President Trump in early 2025 and has raised it again with senior officials in recent weeks, framed as a way to distribute AI's economic gains — returns could reportedly flow to citizens through an "AI dividend." Anthropic, per the report, is not having these conversations. At the other end of the spectrum, Sen. Bernie Sanders is preparing a bill that would effectively claim 50% of the equity of OpenAI, Anthropic, xAI and other labs for a public sovereign wealth fund.

The talks landed two days after the President signed an executive order asking AI companies to give the government early access to their models — and the same week Canada unveiled an AI strategy that includes buying equity stakes in domestic AI startups.

These cap tables already hold hyperscalers, chipmakers, and sovereign funds. A government tranche would be a new species of holder entirely — one whose disclosure obligations, exit behavior, and governance rights have no template in venture documentation. For companies preparing public filings, how such a stake would even be described in an S-1 is an open question. Preliminary talks are just that; nothing reported suggests terms exist. But the direction of interest — states wanting in, not just regulating from outside — is itself a structural shift worth tracking.

Sources: NOTUS · CNBC — the June 2 executive order · Reuters — Canada's AI strategy

Quantinuum's debut — priced above range, closed where it started

The new IPO pipeline produced its first completed data point on Thursday. Quantinuum, the Honeywell-backed quantum computing company, priced its upsized offering at $60 — above its $53–$55 range — raised $1.68 billion, opened at $68, touched $71.35, and closed at $60.38, up 0.63% on the day, for a market value of $15.7 billion, per CNBC.

Read as a single print: demand was real enough to price above range, and the aftermarket gave back the opening pop rather than extending it. For the queue of issuers behind it — SpaceX next week, Anthropic and others with confidential filings pending — a debut that ends flat is a different signal than one that doubles or breaks. It suggests buyers are engaging with offerings at the offered price rather than chasing them after. One print is one print; how QNT trades over the coming weeks may provide more context than its first session.

Source: CNBC — Quantinuum closes flat in Nasdaq debut

Power 20 Watch

"Power 20" refers to Augment's internal ranking of selected private-market activity based on our proprietary methodology. It may not represent the broader private market and should not be treated as a valuation benchmark.

For two years, the largest private names have been marked by primary rounds and secondary indications — numbers negotiated in private, tested against nothing. That era ends on a schedule now. SpaceX trades within weeks at a price the public sets. Anthropic's confidential filing started the SEC's clock on June 1. And the gap between what insiders set and what outsiders publish is no longer hypothetical: $1.77 trillion versus Morningstar's $780 billion is the widest publicly documented disagreement about a single company's worth heading into any listing in memory.

Anthropic spent the week supplying both sides of its own debate. The company published research claiming Claude now authors more than 80% of the code merged into its own codebase and called for top labs to weigh slowing development of self-improving systems — weeks after closing a $65 billion round at a $965 billion post-money valuation. Critics noted the tension; supporters called it consistent with its charter. Either way, a company asking the industry to decelerate while preparing its own public listing is a governance story public investors will eventually price.

The competitive backdrop is repricing too: DeepSeek is reportedly nearing a ¥50 billion ($7.4 billion) raise at a $52–59 billion valuation, per Bloomberg — a reminder that the "no funded rival" assumption embedded in some US lab marks now has a counterexample with Tencent and CATL behind it.

Reported private-company financials and secondary-market indications may be unaudited, incomplete, non-standard, or based on limited transaction activity. They should not be relied upon as fair value, executable pricing, or a basis for any investment decision.

💨 Quick Takes

- More than 1,000 SpaceX employees are negotiating as a bloc ahead of the IPO — Current and former employees representing a reported $20 billion in combined assets are collectively pressing wealth managers for sub-0.5% fees and tax-planning tools, per Bloomberg reporting. Coordinated employee liquidity behavior is one variable to monitor in post-lock-up share supply — and a template OpenAI and Anthropic employees may study.

- Anthropic's self-improvement disclosure draws both alarm and skepticism — The company urged labs to consider slowing development of self-improving systems while disclosing that Claude writes most of its own merged code. Some critics argue the call could advantage incumbents over smaller rivals; the company frames it as consistent with its public-benefit mandate.

- SpaceX won a 35-year property tax exemption for its $55B Terafab chip facility — Grimes County, Texas approved a 100% exemption days before the IPO, over threatened legal action from residents. The fab is central to the AI-infrastructure scenarios that divide the company's bulls from Morningstar's estimate.

- Cloudflare acquired VoidZero, the company behind the Vite JavaScript tooling ecosystem — A strategic-acquirer exit for a developer-tools startup that raised its Series A only last October; the open-source projects stay MIT-licensed.

💰The Funding Lineup

The following financing rounds are included for market context only and are not recommendations or valuation opinions.

- Ramp — $750M Series F at $44B (June 4). Led by Iconiq, GIC, and Ontario Teachers', with Goldman Sachs Alternatives and Morgan Stanley among new backers. The corporate-spend platform reported purchase volume growing ~170% year-over-year in March; the round positions AI-spend governance as fintech's current premium story.

- Supabase — $500M Series F at $10.5B post-money (June 4). GIC led; the valuation roughly doubled in about eight months on AI-app database demand. Structurally notable: the company says employees may sell up to 25% of vested stock in every round — recurring liquidity built into the cap table rather than bolted on later.

- Generalist — $400M Series B at $2B (June 4). Radical Ventures led, with Nvidia backing, for the robotics-foundation-model maker — an indication that investors are extending the pretraining-and-scaling playbook from language to the physical world.

- Flourish — $500M, including $100M from Jeff Bezos, at a reported $2.5B (June 4). The stealth-emerging lab is pursuing brain-inspired "synthetic intelligence" designed to use far less power than LLMs — a structural hedge on the energy economics underwriting today's datacenter buildout.

- Lila Sciences — reportedly in talks for ~$2B at $8.5B pre-money (June 3). CalPERS and Nvidia's NVentures reportedly anchor the Series B for the Flagship-incubated AI-for-science company, whose reported valuation has risen from $1.3 billion in October. AI-for-discovery is becoming its own megaround category, distinct from foundation models. Terms are not final.

- DeepSeek — reportedly nearing ¥50B ($7.4B) at a $52–59B valuation (June 3). Tencent, CATL, and founder Liang Wenfeng reportedly lead what would be one of China's largest startup financings ever — and the first outside capital for a lab that built V3 and R1 without venture money. The round has not closed; terms reportedly remain subject to change.

📈 Data Point of the Day

54%

Anthropic's $50 billion May raise accounted for 54% of the entire world's $92 billion in venture funding that month, per Crunchbase — the second-largest monthly total on record, more than half of it one company. Concentration at that level means headline funding totals have stopped describing the market: May was simultaneously a near-record month and, for most startups outside the AI megacap cluster, an ordinary one. Read the components, not the sum.

Reported private-company financials and secondary-market indications may be unaudited, incomplete, non-standard, or based on limited transaction activity. They should not be relied upon as fair value, executable pricing, or a basis for any investment decision.

Source: Crunchbase News — May 2026 venture funding recap

🎓 Manual

Bookbuilding

A residual value support agreement is a guarantee in which a third party agrees to cover a shortfall if the collateral behind a loan — here, used AI chips — sells for less than the outstanding debt when the borrower can't pay. In the reported Anthropic chip financing, Broadcom is said to be providing this support on the senior tranches, which is what lets lenders treat highly specialized hardware as financeable collateral. The mechanism may allow debt to flow into assets that would otherwise be too illiquid or too fast-depreciating to lend against on their own.

👀 What We're Watching

- SpaceX's debut, possibly June 12. The roadshow opens the week of June 8, with Nasdaq trading under SPCX reportedly possible by week's end. The first public prints against the $135 offer price — and against Morningstar's $780 billion estimate — may provide the clearest read yet on how public buyers treat private-era marks. (CNBC)

- Whether the $36B Anthropic chip financing closes. Apollo and Blackstone's TPU lease-financing deal — with order books open and a close that was anticipated this week — has not been publicly confirmed as finalized. If it closes, it would rank among the largest private credit transactions ever assembled; its final terms may signal how lenders price AI-hardware collateral. (Bloomberg)

- Next steps on government equity stakes in AI labs. The NOTUS report describes preliminary conversations, not terms. Any formalization — or public denial — would carry implications for how AI cap tables are structured and disclosed in eventual filings. (NOTUS)

- DeepSeek's close. The reported ¥50 billion round could be finalized within weeks. A completed financing at a $52–59 billion valuation would put a fresh, externally validated mark on the most prominent Chinese AI lab for the first time. (Bloomberg)

Augment Markets Inc. is a technology company offering software and data services. Brokerage services are offered through Augment Capital LLC, an affiliated broker-dealer and member FINRA/SIPC. Investment advisory services are offered through Augment Advisors LLC, an SEC-registered investment adviser.

Important Disclosures: This material has been prepared for informational purposes only. None of the information provided represents a recommendation, an offer or the solicitation of an offer to buy or sell any security. The information provided does not constitute investment, legal, tax, or accounting advice. You should consult with qualified professionals before making any investment decisions. Investing in private securities involves substantial risk, including the potential loss of principal. Private securities are typically illiquid, have limited pricing transparency, and often require longer holding periods. These investments are available exclusively to qualified accredited investors and offer no guarantee of returns. An IPO or other liquidity event is not guaranteed. Additionally, past performance of private securities does not indicate or predict future results. Share price data are estimates only, based on proprietary data from Caplight and Augment Markets Inc. and its affiliates.

Paul leads editorial at Augment, building Pulse into the private markets' go-to intelligence source. He also develops editorial content strategies for startups and venture capital firms. Previously, he spent 15 years as a business and opinion journalist at The New York Times, Fortune, Fast Company, Reuters, and more. He believes transparency creates liquidity—and that someone should actually publish what private shares are trading for. He lives in Marin with his wife and two rescue dogs, and wishes he had more time to surf.

Learn more

FOR QUALIFIED INSTITUTIONAL AND ACCREDITED INVESTORS ONLY: Under federal securities laws, private market investments on this platform are available exclusively to Institutional and Accredited Investors. Verification of status required before investing. Private investments involve significant risks including illiquidity, potential loss of principal, and limited disclosure requirements. "Augment" refers to Augment Markets, Inc. and its affiliates. Augment Markets, Inc. is a technology company offering software and data services, not a bank or financial institution. Cash Accounts are provided by Modern Treasury Corp. financial institution partners and through Augment's technology. Augment does not act as a money services business, provide money transmission, or serve as a custodian of funds. Funds held in your Cash Account are not FDIC insured unless expressly disclosed. Full terms available in the Augment Cash Account Agreement.Brokerage services are offered through Augment Capital, LLC, an affiliated broker-dealer and member FINRA/SIPC. “Investment accounts” are not brokerage accounts and do not hold customer funds or securities. Investment advisory services are offered through Augment Advisors, LLC, an SEC-registered investment adviser. Registration with the SEC does not imply a certain level of skill or training. Augment and its affiliates do not provide legal or tax advice; consult your attorney or tax professional regarding your specific situation. For additional information, please refer to Augment Advisors, LLC’s Form ADV Part 2A (Firm Brochure) and FINRA BrokerCheck.