The $15 between SpaceX's offering price and its first public trade illustrates how IPO allocation mechanics can affect who has access to the offering price, and not in SpaceX's account.

Deep Dive: How an IPO Actually Works — From Banker Handshake to Opening Bell

On the night of June 11, before a single share traded publicly, a small group at Goldman Sachs and SpaceX sat down with a spreadsheet of investor demand and picked a number: $135. The next morning the stock opened at $150 and closed its first day at $160.95, up 19% — reportedly the largest IPO on record, beating Saudi Aramco's $29.4 billion from 2019 by a wide margin (NPR, NBC News).

Two prices, set about fifteen hours apart, by two processes that have almost nothing to do with each other. Most coverage reads the distance between them as the market discovering what SpaceX is worth. Run through how each price actually gets made and the gap resolves into something more concrete: value moving to a pre-selected set of hands before the public places its first order. Here's the whole sequence, and who captures what along the way.

What the 19% pop is supposed to prove

The clean version of the story goes like this. SpaceX is "worth" whatever the market says it's worth, and on June 12 the market spoke: a little over $160 a share, a $2.2-trillion-plus company. The $135 offering price was just the bankers being careful. The 19% pop proves the deal "worked." Everybody won.

It's a tidy story, and it's how a pop gets reported every time. It also skips the only question that matters if you're trying to understand where the money went: who was allowed to buy at $135, and who had to wait until $150? Those aren't the same people, and the gap between their entry prices is built into the machinery days in advance.

Where the prices actually come from

Follow the company from private to public and you pass through several different price-setting events, each run by a different group under different rules.

The bank. SpaceX hired Goldman Sachs into the "lead left" slot — primary control over allocation, pricing, and institutional outreach — with Morgan Stanley, BofA, Citi, and J.P. Morgan as joint bookrunners and roughly twenty more firms in the syndicate (CNBC). The syndicate's fee on a deal this size generally runs 1–2% of proceeds, which on $75 billion implies somewhere around $750 million to $1.5 billion, typically deducted from offering proceeds or otherwise paid pursuant to the underwriting arrangements (Fortune).

The S-1. Months earlier, SpaceX filed its registration statement with the SEC — audited financials, risk factors, cap table, use of proceeds. No price, no shares sold. Just the legal foundation everything else sits on.

The roadshow. For about two weeks, the company and its bankers pitched institutional investors — mutual funds, sovereign wealth funds, hedge funds — who responded with non-binding indications of how many shares they'd want and at what price. This is "building the book." Goldman's job was to aggregate that demand into a single answer to one question: what will the largest pools of capital actually pay?

Pricing night. The evening before trading, Goldman and SpaceX took the book and set the offering price at $135 (CNBC). At that moment, institutional allocations were locked, SpaceX knew exactly what it had raised, and the cash moved. SpaceX had its $75 billion before one share changed hands in public. That price came out of a room, anchored to institutional demand, negotiated by people with a spreadsheet.

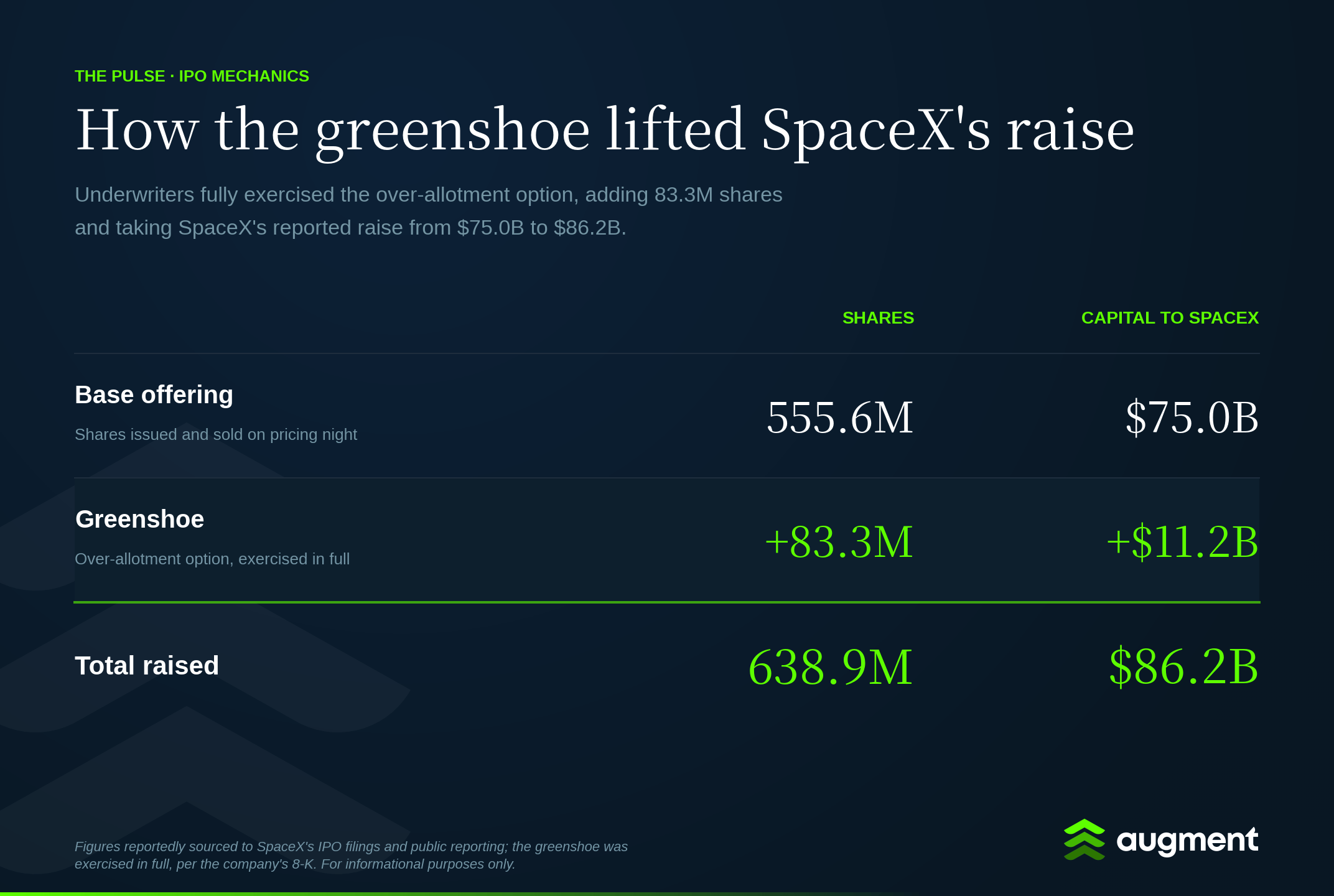

The greenshoe. Here's the mechanism most explainers skip. The syndicate sold roughly 638.9 million shares to institutions on pricing night, but SpaceX only issued 555.6 million. The extra 83.3 million, about 15%, were sold short by the underwriters, these were shares that didn't exist yet. That's the greenshoe, or over-allotment option, and it's standard. The stabilization agent holds a 30-day option to buy those 83.3 million shares from SpaceX at $135 to cover the short.

All figures sourced to SpaceX's filings and the reporting linked in this section. Both numbers are disclosed in the S-1.

With the stock trading well above $135, exercising the option was one potential path: the alternative was buying 83.3 million shares in the open market at a price to cover. Media reports indicate the option was fully exercised, which will be disclosed in an 8-K within 30 days (SEC).

Reported private-company financials and secondary-market indications may be unaudited, incomplete, non-standard, or based on limited transaction activity. They should not be relied upon as fair value, executable pricing, or a basis for any investment decision.

Follow the fifteen dollars

So there are at least three different prices in a single IPO, and the public sees only the last one.

The offering price ($135) is a negotiated number, set in a room, anchored to institutional demand. The opening price ($150) is an auction outcome: on the morning of June 12, the Nasdaq's market maker aggregated every buy and sell order that piled up before the bell and found the level where volume cleared. Heavy buy-side pressure from retail and institutions who got no allocation, thin sell-side supply from the few who could sell — the price that balanced them was $150. The first-day close of $160.95 is a third number, the running tally of all-day trading.

The $15 between $135 and $150 is the part worth slowing down on. Retail bought at the open and paid $150. Institutions allocated the night before paid $135. Follow that $15: the banks earn their fee either way, and SpaceX had already banked its $135, so the gap went to whichever IPO-allocated institutions chose to flip into the open. Most don't. Underwriters track flip rates and generally penalize repeat flippers with worse allocations next time, which is its own quiet form of control. That benefit is not guaranteed, may be affected by lock-ups, allocation restrictions, stabilization activity, market conditions, and investor behavior, and may not be captured by all allocated investors.

Underpricing is a documented regularity in IPOs, studied for decades, and the offering price tends to sit below where the stock first trades. One common explanation is that the gap buys a clean, fully-sold deal and rewards the institutional clients a bank needs for its next mandate. Whatever the cause, the dollars are real, and the people positioned to capture them were chosen on pricing night.

That's the thing the pop obscures. An IPO runs as a sequence of handoffs, private company to bank, bank to institutions, institutions to the public, and each one prints a different price. Being early to the sequence can be economically meaningful when the stock opens above the offering price, and the bank that controls the book decides who gets to be early.

The other door into the building

Which is the part that should interest anyone who isn't a Goldman institutional client.

If the value in an IPO is in being early, then the allocation list is the gate, and the gate is narrow and political. You get the $135 price because you're a fund Goldman wants to keep happy for the next mandate. Everyone else meets the company at $150 or later, on the public tape, after the early value has already been distributed: employees, retail, smaller funds, founders' networks.

The secondary market may be another door into the same building. It's where shares of a company like SpaceX changed hands for years before any of this, at prices set by willing buyers and sellers rather than by a bookrunner's allocation logic. An employee who sold SpaceX on the secondary in 2024, and the fund that bought, were trading the same thing the allocation list monetized on pricing night: access to the company before the public could touch it. The difference is the door isn't gated by league-table politics. That's the structural reason a secondary market exists for late-stage private names at all, and it's why the names still private after SpaceX, the ones Augment tracks, draw the interest they do.

Reported private-company financials and secondary-market indications may be one consideration for eligible investors evaluating private-market opportunities. They should not be relied upon as fair value, executable pricing, or a basis for any investment decision.

Before you call it a giveaway

The cynical read, underpricing as a giveaway to insiders, is too clean, and the other side deserves a fair hearing. The pop is also insurance. SpaceX traded a higher price for certainty: a fully-sold $75 billion offering, locked at $135, with no risk of a broken deal on the largest IPO ever attempted. Seen that way, the $15 is a premium the company paid to de-risk a number with no precedent, and a stable first week is worth more to SpaceX than the last few dollars of proceeds.

And the secondary door charges its own toll. The pre-IPO buyer takes illiquidity, stale and contested marks, thin information, and a holding period of unknown length. The IPO buyer pays in the pop; the secondary buyer pays in everything that comes from owning a private company nobody's required to keep you informed about. Both doors charge admission. The honest question is which toll you'd rather pay, and how early you need to be to think it's worth it.

Sources: NPR (June 11), NBC News (June 12), CNBC (June 3), CNBC (May 19), Fortune (June 11), SEC EDGAR (8-K).

📈 Data Point of the Day

$29.4 billion

The size of the previous record IPO, Saudi Aramco's 2019 listing. SpaceX reportedly raised $75 billion, roughly 2.5x that, in a single offering, and briefly touched a market value above $2.25 trillion intraday on its first day before closing near $2.2 trillion. The prior record stood for nearly seven years.

🎓 Manual

Greenshoe (Over-Allotment Option)

A clause in the underwriting agreement that may let the underwriters sell up to 15% more shares than the company actually issues, then settle the resulting short either by buying the extra shares from the company at the offering price or by buying them back in the open market, generally within 30 days. It takes its name from the Green Shoe Manufacturing Company, which first used the structure in its 1963 IPO. In some cases it gives underwriters a tool to support trading in the days immediately after a listing.

Augment Markets Inc. is a technology company offering software and data services. Brokerage services are offered through Augment Capital LLC, an affiliated broker-dealer and member FINRA/SIPC. Investment advisory services are offered through Augment Advisors LLC, an SEC-registered investment adviser.

Important Disclosures: This material has been prepared for informational purposes only. None of the information provided represents a recommendation, an offer or the solicitation of an offer to buy or sell any security. The information provided does not constitute investment, legal, tax, or accounting advice. You should consult with qualified professionals before making any investment decisions. Investing in private securities involves substantial risk, including the potential loss of principal. Private securities are typically illiquid, have limited pricing transparency, and often require longer holding periods. These investments are available exclusively to qualified accredited investors and offer no guarantee of returns. An IPO or other liquidity event is not guaranteed. Additionally, past performance of private securities does not indicate or predict future results. Share price data are estimates only, based on proprietary data from Caplight and Augment Markets Inc. and its affiliates.

Noel is an engineer at heart and a product builder at Augment, focused on creating tools that bring genuine joy to users. He previously scaled Rubrik’s on-prem technology to the cloud as an early employee and spent time at Google. He’s a serial builder of side projects, ranging from self-destructing notepads to crypto mining tools. He believes that engineering is a craft—and that great products are built at the intersection of technical rigor and user delight. He lives in Austin with his wife, two kids, and their Golden Retriever. He unfortunately maintains an unironic, shameless love for Nickelback.

Learn more

FOR QUALIFIED INSTITUTIONAL AND ACCREDITED INVESTORS ONLY: Under federal securities laws, private market investments on this platform are available exclusively to Institutional and Accredited Investors. Verification of status required before investing. Private investments involve significant risks including illiquidity, potential loss of principal, and limited disclosure requirements. "Augment" refers to Augment Markets, Inc. and its affiliates. Augment Markets, Inc. is a technology company offering software and data services, not a bank or financial institution. Cash Accounts are provided by Modern Treasury Corp. financial institution partners and through Augment's technology. Augment does not act as a money services business, provide money transmission, or serve as a custodian of funds. Funds held in your Cash Account are not FDIC insured unless expressly disclosed. Full terms available in the Augment Cash Account Agreement.Brokerage services are offered through Augment Capital, LLC, an affiliated broker-dealer and member FINRA/SIPC. “Investment accounts” are not brokerage accounts and do not hold customer funds or securities. Investment advisory services are offered through Augment Advisors, LLC, an SEC-registered investment adviser. Registration with the SEC does not imply a certain level of skill or training. Augment and its affiliates do not provide legal or tax advice; consult your attorney or tax professional regarding your specific situation. For additional information, please refer to Augment Advisors, LLC’s Form ADV Part 2A (Firm Brochure) and FINRA BrokerCheck.