.jpeg)

The confidential filing is at the SEC. We built our own from leaked financials, tender offer docs, and government contract databases — before anyone else sees the real thing.

Thursday Deep Dive: Reverse-Engineering the SpaceX S-1

SpaceX filed its confidential S-1 with the SEC yesterday, setting the stage for what could be the largest initial public offering in history — a listing reportedly targeting a $1.75 trillion valuation and raising as much as $75 billion. For context, that would more than double the $29.4 billion Saudi Aramco raised in 2019.

Nobody outside SpaceX, its bankers, and the SEC has seen that filing. But SpaceX is one of the most closely tracked private companies on Earth. Between leaked financials, tender offer documents, analyst estimates, partnership disclosures, and government contract databases, there is an unusual amount of public data circulating about a company that has never published a single quarterly report.

Here's the number that stopped us: SpaceX's implied valuation has increased 4.4x in under 12 months — from $400 billion at last July's tender to the reported $1.75 trillion IPO target. Saudi Aramco moved 1.2x over the same pre-IPO window. Whether that repricing is backed by fundamentals or narrative momentum is the single most important question the S-1 will answer.

So we did something we've never done before: we reverse-engineered the S-1 nobody's seen yet.

What follows is an exercise in structured estimation — not the actual filing. Every number below is drawn from publicly reported data (sourced inline) or is explicitly marked as an estimate. Think of it as the analyst's sketchpad before the real document goes public. When SpaceX releases its S-1 — at least 15 days before the expected late-summer 2026 road show — you'll have a framework to read it against.

I. Business Overview: Five Companies in a Trench Coat

The first surprise in any SpaceX S-1 would be the segment reporting. This isn't one business — it's at least four, stitched together under a single cap table and now, since the February 2026 xAI merger, arguably five.

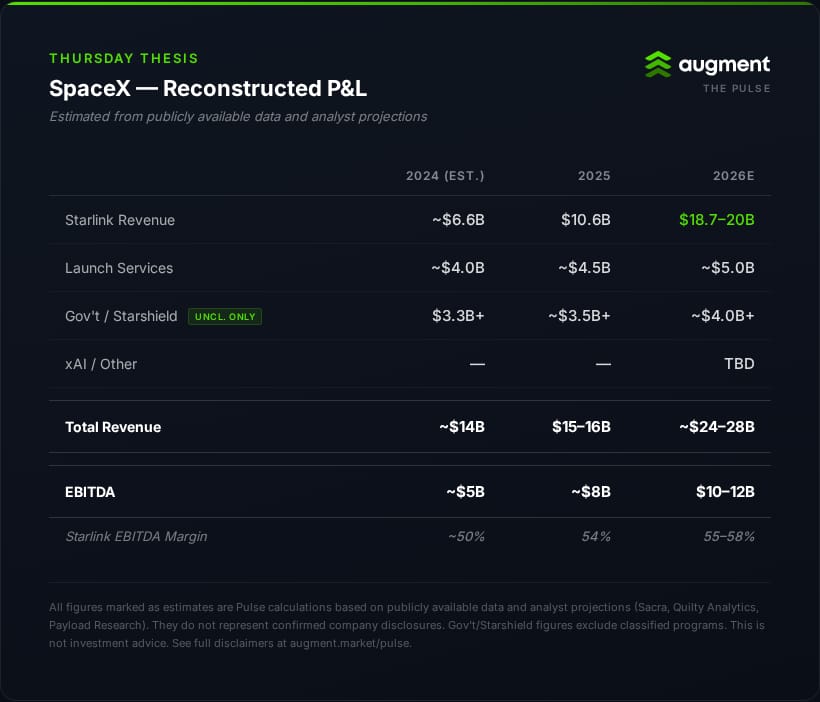

Starlink (Satellite Internet) — the cash engine. Sacra estimates Starlink generated $10.6 billion in 2025 revenue at a 54% EBITDA margin, accounting for roughly two-thirds of total company revenue. Quilty Analytics projectsStarlink could reach $18.7–20 billion in 2026 revenue as subscriber counts push past 10 million users globally.

Launch Services — the legacy franchise. Falcon 9 remains the workhorse of the global launch market, with 165 launches in 2025 and an estimated 140–145 planned for 2026. At roughly $62 million per Falcon 9 mission, this segment likely contributes $4–5 billion in annual revenue — significant, but increasingly secondary to Starlink.

Starshield (Government/Defense) — the classified wildcard. SpaceX has received approximately $22 billion in cumulative federal contracts, with $3.3 billion in unclassified government revenue in 2024 alone — and that figure excludes classified programs. A $1.8 billion classified contract to build hundreds of spy satellites, revealed in 2023, hints at a defense revenue stream that may be substantially larger than public figures suggest. The PLEO program ceiling grew from $900 million to $13 billion — a signal the Pentagon views Starshield as infrastructure, not experiment.

Starship — the capital-intensive bet. SpaceX has reportedly invested over $5 billion in Starship R&D through early 2024, with the program costing approximately $4 million per day as of 2024. Elon Musk has said total development costs will fall between $5 billion and $10 billion. This is the segment that would dominate the "Use of Proceeds" section of any S-1 — IPO capital reportedly earmarked for an "insane flight rate" for Starship, orbital data centers, and a lunar base.

xAI — the February addition. The all-stock triangular merger, valuing xAI at $250 billion and the combined entity at $1.25 trillion, brought Grok's large-language models and investors including Nvidia, Cisco, and sovereign wealth funds into the SpaceX shareholder base. This segment adds AI revenue but also complexity — expect the S-1 to spend considerable ink explaining how "orbital data centers" justify combining a rocket company with an AI lab.

II. The Financials We Can Estimate

Here's what a reconstructed P&L might look like, based on publicly available data:

The story the numbers tell: Starlink's margin expansion is funding everything else. The consumer satellite business is approaching software-like economics — high fixed cost, near-zero marginal cost per additional subscriber — while generating the cash flow to subsidize Starship development and absorb the xAI integration. A real S-1 would likely show Starship as a massive drag on net income, offset by Starlink's accelerating profitability.

III. The Cap Table: More Complex Than You'd Think

A SpaceX S-1 would reveal one of the most scrutinized cap tables in private market history. What we know from public reporting:

Elon Musk holds approximately 42% equity and ~79% voting control through a dual-class share structure. The xAI merger converted xAI shares at a 0.1433 ratio into SpaceX stock, likely diluting existing holders while reinforcing Musk's control.

Institutional holders include Alphabet (~7.5%), Founders Fund (~10.4%), Fidelity (~10.2%), plus Sequoia Capital and Andreessen Horowitz at smaller stakes. Post-merger, Nvidia, Cisco, Qatar Investment Authority, and Abu Dhabi's MGX joined the register via their xAI positions.

Employees hold a meaningful but undisclosed stake across options and RSUs. With an estimated ~18,000 employees, the IPO would create a significant liquidity event. SpaceX has historically run semi-annual tender offers — the December 2025 tender at $421/share ($800B valuation) doubled the $212/share price from July 2025 ($400B valuation).

The valuation walk: $400B (July '25) → $800B (Dec '25) → $1.25T (xAI merger, Feb '26) → $1.75T (reported IPO target). That's the 4.4x repricing in under a year. For secondary market participants, the question isn't whether early holders made money — it's what the entry price implies about future returns at the IPO target.

IV. Risk Factors: What the S-1 Would Have to Disclose

Every S-1 contains a risk factors section. SpaceX's would likely be unusually dense. Based on public record, expect disclosures around:

Regulatory dependency. SpaceX's launch cadence depends entirely on FAA licensing. The company has publicly criticized the pace of regulatory review, arguing "it takes longer to do the government paperwork to license a rocket launch than it does to design and build the actual hardware." Environmental lawsuits over Starship operations at Boca Chica, while dismissed in September 2025, signal ongoing friction.

Key-person risk. Musk's 79% voting control and role across SpaceX, Tesla, xAI, X, Neuralink, and The Boring Company would be a multi-page risk factor. No public company of this scale has this degree of single-person dependency and cross-entity complexity.

Classified revenue opacity. Investors in a public SpaceX would have limited visibility into Starshield's classified programs — a meaningful portion of government revenue that can't be fully disclosed in SEC filings.

Starship execution risk. The entire "Use of Proceeds" thesis depends on Starship achieving operational reliability at scale. The program remains developmental, with no commercial payload launches completed as of filing.

xAI integration risk. Combining an AI company valued at $250 billion with a rocket company requires demonstrating synergies that, as of now, are largely theoretical ("orbital data centers").

V. The Private Markets Angle

For secondary market observers, the simulated S-1 framework reveals several structural dynamics:

The liquidity premium question. SpaceX shares traded at $595–674 on secondary platforms as of March 2026, implying valuations well north of $1 trillion. The gap between secondary pricing and the $1.75T IPO target suggests the market is pricing in both a liquidity premium at IPO and continued operational momentum. Whether that premium materializes or compresses depends on how the actual S-1 numbers compare to the estimates above.

Segment visibility changes everything. Today, secondary market participants are buying "SpaceX" as a single bet. Once the S-1 publishes segment reporting, the market can disaggregate Starlink's cash generation from Starship's cash consumption and xAI's uncertain contribution. That transparency could meaningfully reprice how different investor types value the combined entity.

The tender-to-IPO bridge. The December 2025 tender at $421/share represented an $800B valuation. The IPO targets $1.75T — a 119% premium to the last tender. Historically, late-stage tender-to-IPO premiums of this magnitude are rare for companies of this scale. The S-1 will be the first opportunity for the market to test whether the intervening repricing was justified by fundamentals or driven by narrative momentum.

VI. The Counterargument

The bull case writes itself — Starlink's margin profile, launch monopoly economics, and government tailwinds make SpaceX genuinely exceptional. But a skeptic reading the same data would note:

The $1.75 trillion target values SpaceX at roughly 65–70x estimated 2026 EBITDA. Even at the high end of revenue estimates, that's a premium that assumes years of compounding growth with minimal margin compression. The xAI merger added $250 billion in valuation for a business whose revenue contribution to the combined entity remains unclear. And Starship — the program that justifies the "Use of Proceeds" narrative and much of the long-term vision — has not yet completed a commercial mission.

None of that means the valuation is wrong. It means the S-1, when it goes public, will be the most important document for stress-testing which parts of the SpaceX narrative are backed by cash flow and which are backed by conviction.

We'll be reading it closely.

📈Data Point of the Day

4.4x

The multiple by which SpaceX's implied valuation increased from July 2025 ($400B tender offer) to the reported IPO target ($1.75T), a span of approximately 12 months. For comparison, Saudi Aramco's valuation moved roughly 1.2x from its final pre-IPO assessment to listing price. Whether SpaceX's repricing reflects fundamental improvement or pre-IPO narrative escalation is precisely the question the S-1 will answer.

🎓 Manual

Dual-Class Share Structure — A corporate structure in which a company issues two classes of stock with different voting rights. Typically, one class (held by founders and insiders) carries significantly more votes per share than the other (sold to public investors). SpaceX's structure reportedly gives Elon Musk ~79% voting control with ~42% economic ownership — a gap that would be a focal point for governance-focused institutional investors evaluating the IPO.

Augment Markets Inc. is a technology company offering software and data services. Brokerage services are offered through Augment Capital LLC, an affiliated broker-dealer and member FINRA/SIPC. Investment advisory services are offered through Augment Advisors LLC, an SEC-registered investment adviser.

Important Disclosures: This material has been prepared for informational purposes only. None of the information provided represents a recommendation, an offer or the solicitation of an offer to buy or sell any security. The information provided does not constitute investment, legal, tax, or accounting advice. You should consult with qualified professionals before making any investment decisions. Investing in private securities involves substantial risk, including the potential loss of principal. Private securities are typically illiquid, have limited pricing transparency, and often require longer holding periods. These investments are available exclusively to qualified accredited investors and offer no guarantee of returns. An IPO or other liquidity event is not guaranteed. Additionally, past performance of private securities does not indicate or predict future results. Share price data are estimates only, based on proprietary data from Caplight and Augment Markets Inc. and its affiliates.

Paul leads editorial at Augment, building Pulse into the private markets' go-to intelligence source. He also develops editorial content strategies for startups and venture capital firms. Previously, he spent 15 years as a business and opinion journalist at The New York Times, Fortune, Fast Company, Reuters, and more. He believes transparency creates liquidity—and that someone should actually publish what private shares are trading for. He lives in Marin with his wife and two rescue dogs, and wishes he had more time to surf.

Learn more

FOR QUALIFIED INSTITUTIONAL AND ACCREDITED INVESTORS ONLY: Under federal securities laws, private market investments on this platform are available exclusively to Institutional and Accredited Investors. Verification of status required before investing. Private investments involve significant risks including illiquidity, potential loss of principal, and limited disclosure requirements. "Augment" refers to Augment Markets, Inc. and its affiliates. Augment Markets, Inc. is a technology company offering software and data services, not a bank or financial institution. Cash Accounts are provided by Modern Treasury Corp. financial institution partners and through Augment's technology. Augment does not act as a money services business, provide money transmission, or serve as a custodian of funds. Funds held in your Cash Account are not FDIC insured unless expressly disclosed. Full terms available in the Augment Cash Account Agreement.Brokerage services are offered through Augment Capital, LLC, an affiliated broker-dealer and member FINRA/SIPC. “Investment accounts” are not brokerage accounts and do not hold customer funds or securities. Investment advisory services are offered through Augment Advisors, LLC, an SEC-registered investment adviser. Registration with the SEC does not imply a certain level of skill or training. Augment and its affiliates do not provide legal or tax advice; consult your attorney or tax professional regarding your specific situation. For additional information, please refer to Augment Advisors, LLC’s Form ADV Part 2A (Firm Brochure) and FINRA BrokerCheck.