SpaceX filing unveiled; IPO pipeline comes into focus

.svg)

.jpeg)

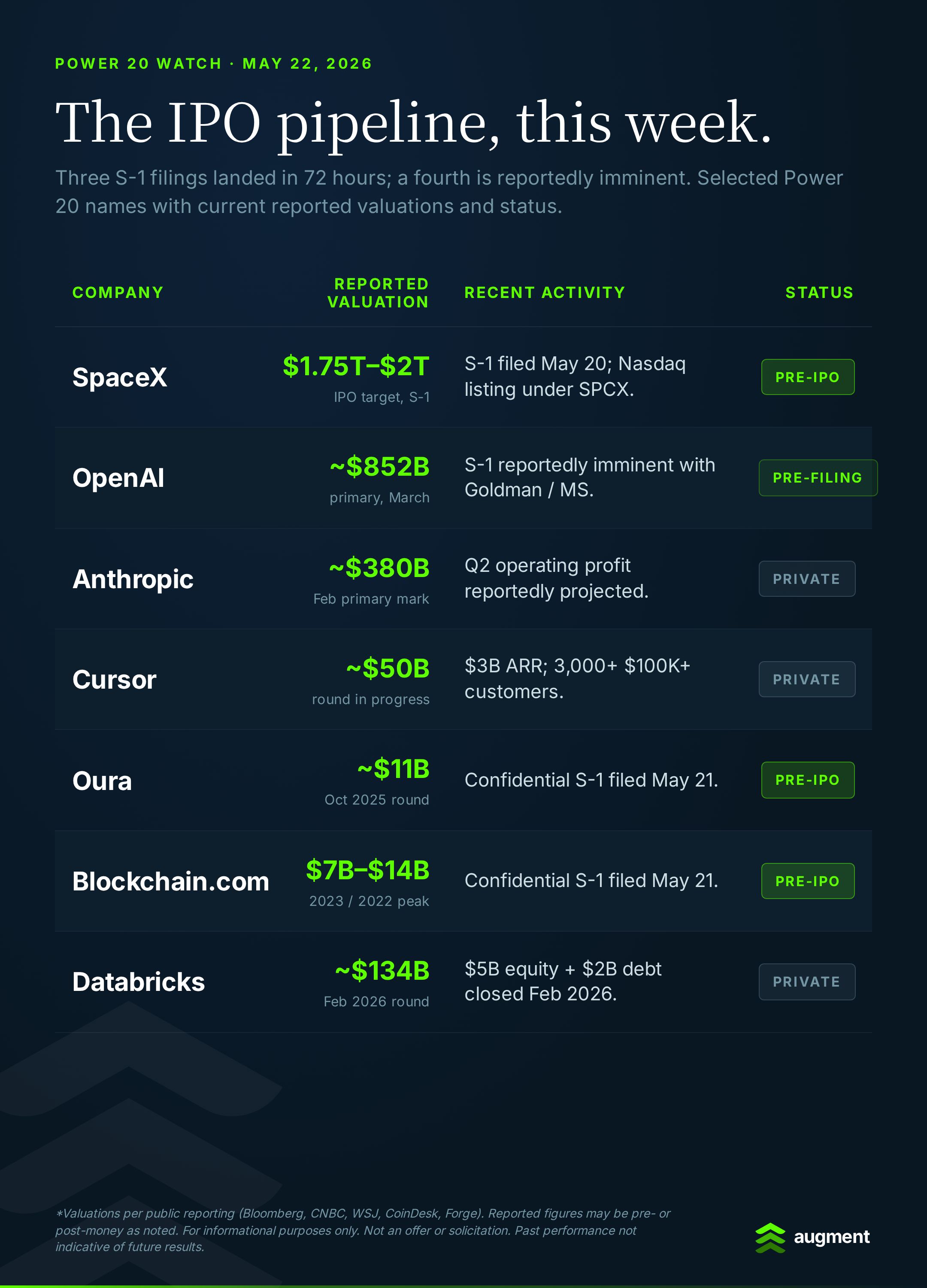

Three S-1 filings landed inside roughly 72 hours this week — SpaceX publicly, with Oura and Blockchain.com both filing confidentially the same day. A fourth, OpenAI, is reportedly preparing a confidential filing imminently. Separately, Anthropic told investors it expects its first operating profit this quarter on $10.9 billion in revenue — a number that resets the AI-lab comp set.

The Big Story: Three S-1s in 72 Hours, a Fourth Imminent

The week began with SpaceX filing publicly on Wednesday afternoon for a Nasdaq listing under the ticker SPCX, targeting a $75 billion raise at a reported valuation between $1.75 trillion and $2 trillion. That would put the raise at more than 2.5 times Saudi Aramco's $29.4 billion debut and make it the largest IPO on record. The S-1 disclosed roughly $19 billion in 2025 revenue, an operating loss of about $5 billion, and a dual-class structure that gives Elon Musk 85.1% of voting power. Starlink is on track to produce more than 70% of revenue. The financials were rebuilt to include xAI, which SpaceX acquired in February.

Two more issuers confirmed their own filings the next day. Oura, the smart-ring maker, filed confidentially on Thursday; its last private mark was $11 billion in October. Blockchain.com — once valued at $14 billion at the 2022 crypto peak — also filed confidentially Thursday, targeting a 2026 listing. Behind them, CNBC reported Wednesday that OpenAI is preparing to file a confidential S-1 with Goldman Sachs and Morgan Stanley as soon as Friday, targeting a Q4 listing. As of Thursday evening, no public confirmation that the OpenAI filing has been submitted.

The three confirmed filings span space, consumer hardware, and crypto. Different categories, different scales, one calendar — with the AI lead reportedly queued up behind. The reading-between-the-lines question for private-market participants is whether this is the start of a real reopening or a narrow window that closes around SpaceX's pricing. The two preceding cycles — 2014's Alibaba-driven moment and 2021's everything-IPOs-now phase — both showed the same pattern early: a single megacap filing draws several mid-size issuers off the bench, then the band either holds and broadens or pricing fails on the lead and the rest pull their books. Watch the pre-pricing reads on SpaceX over the next two weeks. The cohort behind it has positioned itself to move with the same tape.

Sources: Bloomberg (May 20), CNBC (May 20), Bloomberg (May 21), CoinDesk (May 21), Kiplinger (May 20)

Anthropic's Numbers Reset the AI-Lab Comp Set

Anthropic told investors this week that it expects to post its first operating profit this quarter — $559 million on $10.9 billion of Q2 revenue, according to The Wall Street Journal. Q1 revenue was $4.8 billion. The projection more than doubles the top line quarter-over-quarter and represents a sharp reversal from last summer, when the company told investors it did not expect full-year profitability until 2028. Anthropic itself cautions that subsequent quarters may not remain profitable given the compute commitments coming due.

One private-market interpretation is the potential comparison between Anthropic and OpenAI, though the companies differ in business mix, cost structure, capital commitments, and disclosure quality. The Information reported Q1 figures showing OpenAI at roughly $5.7 billion in revenue with an operating margin of negative 122%. Anthropic was roughly a billion dollars behind on revenue in Q1 — and is now projecting a quarter where it earns operating profit while OpenAI's losses widen. OpenAI's primary mark is roughly $852 billion as of its March round; the Forge clearing price on OpenAI sits in the same neighborhood. Anthropic's secondary prints have been running materially above its $380 billion Series G mark from February.

This is the closest the secondary market has come to having two AI labs of comparable scale priced against actually-reported financials. The market has been pricing on revenue-growth assumptions; it now has to price against a profitability divergence. That changes the comp set for every AI lab behind them on the cap table.

Sources: WSJ (May 20), The Information (May 20), Forge OpenAI page

Cursor Hits $3B ARR

Bloomberg reported Thursday that Cursor's annualized revenue reached $3 billion in late April, up from a $2 billion run-rate in February. The company now has more than 3,000 customers paying at least $100,000 a year for its software. That cohort alone implies a $300 million-plus annualized contribution from the top tier of accounts. The reporting comes in the context of Cursor's reported $2 billion funding round at a $50 billion valuation, which TechCrunch flagged in April.

The structural read: AI-software unit economics at the application layer are starting to look distinct from the infrastructure layer's. Cursor sits on top of the labs' models and bundles them into a developer workflow. Each marginal user is a marginal inference call to Anthropic or OpenAI, where Cursor pays cost. The fact that the company has tripled its revenue run-rate inside seven months while reportedly operating at scale suggests that the gross-margin question — long the bear case on AI-application companies — has at least one working answer. Whether the model generalizes to other categories is the question that pricing across the AI-application cohort will resolve over the next year.

Sources: Bloomberg (May 21), TechCrunch (April 17)

Reported private-company financials and secondary-market indications may be unaudited, incomplete, non-standard, or based on limited transaction activity. They should not be relied upon as fair value, executable pricing, or a basis for any investment decision.

Power 20 Watch

"Power 20" refers to Augment's internal ranking of selected private-market activity (Methodology). It may not represent the broader private market and should not be treated as a valuation benchmark.

If SpaceX prices $75 billion in mid-June and OpenAI files a public S-1 in Q3 at a $1 trillion-plus target, US equity markets will be asked to absorb something north of $100 billion in fresh issuance from two names inside roughly four months. For comparison, the entire 2021 IPO peak — characterized by 30-plus tech listings of varying quality — cleared roughly $100 billion in aggregate. The 2026 setup, as currently reported, is the inverse: two listings absorbing more capital than that whole cohort.

The Power-20 secondary tape has been the leading indicator for that capacity question for a year. Recent public and confidential filings appear to align with themes that have been visible in parts of the secondary market.

Click to enlarge

The non-obvious read isn't whether the deals price. It's whether the band holds across categories. If SpaceX prices cleanly and Oura prices cleanly, the read is that the window is broad — accredited capital is willing to absorb both a $1.8T space-and-AI conglomerate and an $11B consumer-hardware name at the same time. If SpaceX prices clean and Oura's book softens, the band has narrowed back to the AI / strategic-asset cohort. One market signal to monitor coming out of June.

💨 Quick Takes

- The Anthropic / Blackstone / Hellman & Friedman services JV made its first acquisition: Fractional AI — Fractional reportedly ended a competing arrangement with OpenAI to take the deal. The JV that The Pulse covered on May 5 is now an active strategic acquirer in the AI-services market. Additional acquisitions, if they occur, may provide more context on the categories strategic buyers are prioritizing.

- Trump postponed the AI / cybersecurity executive order at the eleventh hour — Lab CEOs were reportedly already en route to the signing. The order would have required model labs to share frontier models with the government 90 days pre-release; Trump cited a desire not to "get in the way" of the US AI lead. The regulatory regime around private-market AI valuations remains in flux.

- Commerce Department to award $2B to nine quantum-computing firms and take equity stakes — IBM gets the largest single award ($1B); private names PsiQuantum, Atom Computing, Quantinuum, and Infleqtion are in the cohort. Government-as-equity-investor is now reportedly active in 21–23 private companies. The template is a real new variable for late-stage cap tables.

💰The Funding Lineup

The following financing rounds are included for market context only and are not recommendations or valuation opinions.

Six rounds from the past week worth tracking. Mixed by sector to show what investors are actually pricing right now — not the IPO names everyone is already watching.

- Hark — $700M Series A at $6B post-money (May 21). Brett Adcock's third venture (after Vettery and Figure AI) is building "personalized intelligence" hardware. Parkway Venture Capital led, with Nvidia, AMD Ventures, Intel Capital, Qualcomm Ventures, and Salesforce Ventures participating. Five chip vendors on a single Series A cap table is the surprise — and a tell about how much hardware-AI distribution risk the silicon side is willing to underwrite at the same time.

- Modal Labs — $355M Series C at $4.65B (May 21). Serverless AI inference. General Catalyst and Redpoint co-led. Annualized revenue reportedly around $300 million, up from $60 million in September — five times in six months. The valuation is up roughly 4x from $1.1 billion in the fall. AI-inference infrastructure keeps re-rating faster than the cycle would normally support.

- Armada — $230M Series B at $2B pre-money (May 19). Modular AI data centers and satellite-enabled edge compute. Overmatch and BlackRock co-led, with Johnson Controls coming in as a strategic investor under a framework agreement to build a 400,000-square-foot Arizona factory. Customer bookings reportedly up 540% year-over-year. The picks-and-shovels of the Thursday-edition capex thesis — and a data point that defense and energy buyers are sourcing AI infrastructure outside the hyperscalers.

- SendCutSend — $110M at $1B unicorn valuation (May 19). On-demand custom manufacturing — laser cutting, CNC machining, parts delivered in 24 hours. Sequoia, Paradigm, and the Collison brothers (Stripe co-founders) co-led. Reported $200 million in revenue across 100,000 business customers, three US factories running 24/7. The unicorn list this week was not all AI. Domestic manufacturing reshoring is putting up actual unit economics.

- Nourish — $100M Series C (May 19). The largest dietitian-led virtual metabolic clinic, with a network of more than 10,000 registered dietitians across all 50 states. Menlo Ventures led, with Thrive, Index, J.P. Morgan Growth Equity, Maverick, and Y Combinator participating. The pitch sits on top of the GLP-1 prescribing wave — dietitians as the long-tail clinical layer attached to weight-loss-drug care. Healthcare AI commands real growth-stage capital, channeled through condition-specific clinical workflows.

- Moment — $78M Series C (May 19). AI operating system for investment management. Index Ventures led, with a16z and Avra participating. Edward Jones, Hightower, and LPL Financial reportedly use the platform; aggregate client assets across user firms have grown from roughly $3 trillion to over $10 trillion since the Series B last July. AI infrastructure for wealth management — the vertical-AI thesis applied to one of the most fee-sensitive parts of finance.

📈 Data Point of the Day

3,000

That's the number of customers Cursor has paying at least $100,000 a year for its software on an annualized basis, per Bloomberg's Thursday reporting. That single tier implies a contribution above $300 million annualized — before counting any smaller plan. The AI-application layer's unit-economics question has at least one working data point.

Source: Bloomberg (May 21)

🎓 Manual

Lock-up Period

The contractual window after an IPO during which insiders, employees, and pre-IPO investors are restricted from selling their shares. The standard runs 180 days from pricing, though some recent listings have used staggered releases or shorter windows tied to specific holder classes. For secondary-market participants, the lock-up calendar is an inflection point worth tracking: clearing prices on pre-IPO names may converge toward — or diverge sharply from — the public mark as expiry approaches and supply assumptions reset.

👀 What We're Watching

- The OpenAI confidential S-1 actually landing. WSJ and CNBC's sourcing points to as soon as Friday; if it slips into next week, the timing implication is that the underwriters and the SEC are still finalizing disclosure structure on a transaction with reported losses of roughly $14 billion projected for the calendar year. Public S-1 then typically follows three weeks before debut. (CNBC, May 20)

- The SpaceX index-demand math. A $1.75T–$2T listing at IPO would not initially qualify for the S&P 500 (which requires US incorporation in good standing and four quarters of profitability) but would likely be eligible for the Nasdaq-100 and several Russell indices on day one. Forced index buying from a single new entrant of that size has no real historical parallel; the absorption mechanics will be visible in the secondary tape on the names sized closest to it. (Kiplinger, May 20)

- Whether the mid-cap IPO window opens behind the lead. Oura at $11B and Blockchain.com (last private mark around $7B) are the first non-decacorn confidential filings of the cycle. If both price cleanly, the band of issuers preparing to follow them through the queue expands materially. If the lead clears but the mid-caps slip, the read is that the window is narrow and AI / strategic-asset specific. (Bloomberg, May 21 / CoinDesk, May 21)

- The Anthropic profitability question rolling forward. Q2 is projected at first operating profit; Anthropic itself flagged that subsequent quarters may not remain profitable given compute commitments coming due. Whether Q3 holds the line or reverts to operating losses will be one of the cleanest reads on whether AI-lab profitability is a structural inflection or a one-quarter print. (WSJ, May 20)

Augment Markets Inc. is a technology company offering software and data services. Brokerage services are offered through Augment Capital LLC, an affiliated broker-dealer and member FINRA/SIPC. Investment advisory services are offered through Augment Advisors LLC, an SEC-registered investment adviser.

Important Disclosures: This material has been prepared for informational purposes only. None of the information provided represents a recommendation, an offer or the solicitation of an offer to buy or sell any security. The information provided does not constitute investment, legal, tax, or accounting advice. You should consult with qualified professionals before making any investment decisions. Investing in private securities involves substantial risk, including the potential loss of principal. Private securities are typically illiquid, have limited pricing transparency, and often require longer holding periods. These investments are available exclusively to qualified accredited investors and offer no guarantee of returns. An IPO or other liquidity event is not guaranteed. Additionally, past performance of private securities does not indicate or predict future results. Share price data are estimates only, based on proprietary data from Caplight and Augment Markets Inc. and its affiliates.

Paul leads editorial at Augment, building Pulse into the private markets' go-to intelligence source. He also develops editorial content strategies for startups and venture capital firms. Previously, he spent 15 years as a business and opinion journalist at The New York Times, Fortune, Fast Company, Reuters, and more. He believes transparency creates liquidity—and that someone should actually publish what private shares are trading for. He lives in Marin with his wife and two rescue dogs, and wishes he had more time to surf.

Learn more

FOR QUALIFIED INSTITUTIONAL AND ACCREDITED INVESTORS ONLY: Under federal securities laws, private market investments on this platform are available exclusively to Institutional and Accredited Investors. Verification of status required before investing. Private investments involve significant risks including illiquidity, potential loss of principal, and limited disclosure requirements. "Augment" refers to Augment Markets, Inc. and its affiliates. Augment Markets, Inc. is a technology company offering software and data services, not a bank or financial institution. Cash Accounts are provided by Modern Treasury Corp. financial institution partners and through Augment's technology. Augment does not act as a money services business, provide money transmission, or serve as a custodian of funds. Funds held in your Cash Account are not FDIC insured unless expressly disclosed. Full terms available in the Augment Cash Account Agreement.Brokerage services are offered through Augment Capital, LLC, an affiliated broker-dealer and member FINRA/SIPC. “Investment accounts” are not brokerage accounts and do not hold customer funds or securities. Investment advisory services are offered through Augment Advisors, LLC, an SEC-registered investment adviser. Registration with the SEC does not imply a certain level of skill or training. Augment and its affiliates do not provide legal or tax advice; consult your attorney or tax professional regarding your specific situation. For additional information, please refer to Augment Advisors, LLC’s Form ADV Part 2A (Firm Brochure) and FINRA BrokerCheck.