.jpeg)

Thoma Bravo — the world's largest software buyout firm — says the market has the AI-disruption story wrong. Software fundamentals are intact. The real divide is between easily-replaced point solutions and mission-critical, compliance-heavy systems that AI won't touch. They're buying. Private markets investors should pay attention.

Thursday Thesis: Not All Software Is Dying

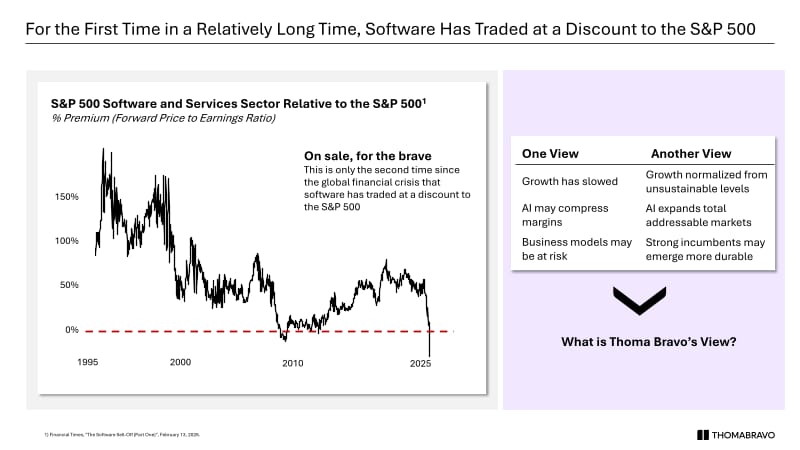

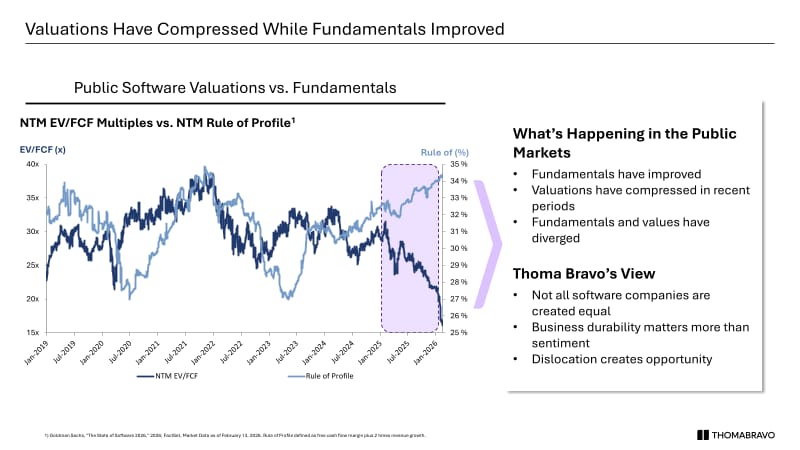

The "SaaSpocalypse" narrative is everywhere right now. The iShares software ETF (IGV) is down roughly 30% from its September 2025 peak. Public software companies — names like Salesforce, Workday, and Atlassian — have shed trillions in combined market cap since early February. Software now trades at a discount to the broader S&P 500 for only the second time since the 2008 financial crisis.

For context: software has commanded a valuation premium over the market for nearly every year of the past two decades. That premium is gone.

The narrative driving the selloff is real and worth taking seriously: if AI agents can handle knowledge work autonomously, the per-seat SaaS licensing model — which grew for 20 years by tracking headcount expansion — faces genuine structural pressure. One Anthropic product launch in February reportedly triggered a single-day wipeout north of $285 billion in software market cap.

But this week, the firm that arguably knows enterprise software better than anyone went public with a different read.

What Thoma Bravo Said

Thoma Bravo — $183 billion in assets under management, 565+ software transactions across 40 years, the largest software-focused buyout firm on the planet — held its annual LP meeting in Miami last week. Managing Partner Holden Spaht shared slides and commentary that pushed back directly on the market's blanket AI-disruption thesis.

A few data points Spaht cited deserve attention:

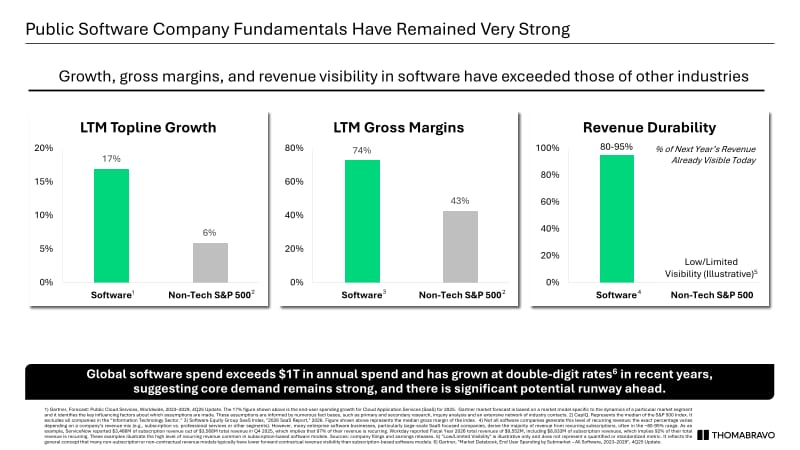

Public SaaS companies grew their top line at roughly 17% last year. The rest of the S&P 500 grew at 6%. Gross margins in software run around 74%, versus 43% for non-tech S&P 500 companies. And 80–95% of next year's revenue for a typical software business is already under contract today.

Those are not the numbers of a sector in distress.

Spaht's explanation for the fundamental-valuation disconnect is worth sitting with. From his post: the revenue deceleration in software between 2022 and 2025 wasn't AI's fault — it was interest rates and COVID-era overselling catching up with the sector. The market was slow to recognize the hangover, then overcorrected on AI disruption fears before the disruption has actually shown up in business performance data.

His conclusion: Thoma Bravo sees a major buying opportunity in software right now.

The Distinction That Matters

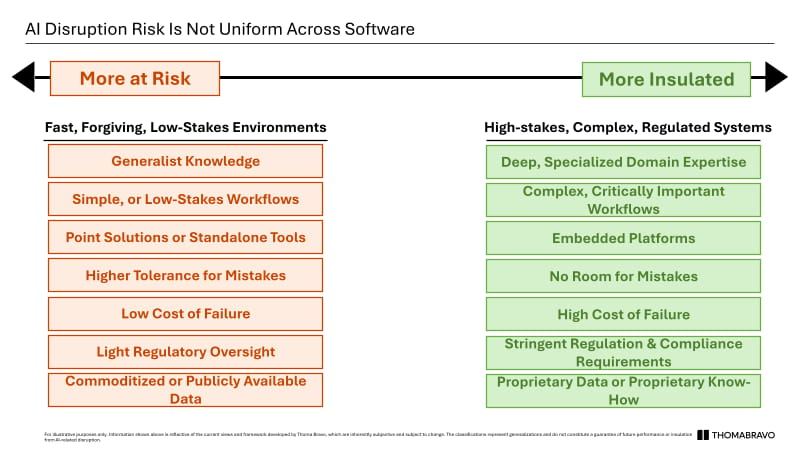

The more important part of Spaht's analysis isn't the macro case for software — it's the line he draws between two fundamentally different categories of software business.

Vulnerable: companies built around generalist knowledge domains, simplified workflows, light regulatory oversight, and limited switching costs. Think: a point solution that automates one thing a human used to do. If AI can do that thing equally well, the product disappears.

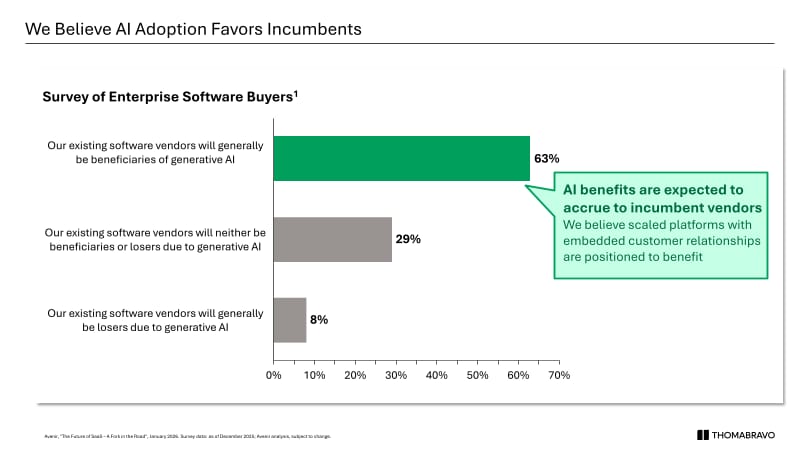

Protected: companies built around deep domain expertise, zero-tolerance-for-error workflows, heavy compliance requirements, and embedded cross-system integration. Think: the software that manages aircraft maintenance records, validates pharmaceutical manufacturing processes, or runs a hospital's billing compliance. Getting it wrong has serious legal, financial, or safety consequences. These systems aren't being ripped out to test a chatbot.

This taxonomy maps almost perfectly to what the public markets are already showing, though the market is applying it bluntly. Public SaaS valuation data from March 2026 shows design and engineering software, data infrastructure, and mission-critical vertical applications trading at significant premiums — while sales automation, content creation tools, and "future of work" software have been hit hardest. Workday and Paycom each missed guidance, and both fell sharply. Meanwhile, Palantir — which operates deep inside defense and intelligence infrastructure with zero tolerance for error — has posted Rule of 40 scores north of 100.

The market is starting to price the distinction. Thoma Bravo is betting it hasn't priced it enough.

The Private Markets Angle

Here's where it gets interesting for secondary investors.

Thoma Bravo has deployed this thesis in real capital, not just LP meeting slides. Recent take-privates include Dayforce (human capital management, $12.3 billion), Olo (restaurant software, $2 billion), and Verint (compliance and workforce intelligence, $2 billion). These are all businesses with the characteristics Spaht described: mission-critical workflows, regulatory complexity, embedded integrations.

The public market's indiscriminate software selloff has also created a notable pattern in PE activity. Analysts covering enterprise software M&A now expect 5–10% of the public SaaS universe to be acquired in 2026 — with PE buyers offering premiums of 30–50% above depressed trading prices. Deal flow in Q1 2026 is the highest since 2021.

For secondary market participants, this dynamic has two implications worth watching.

First, any high-quality software company that went private with a PE sponsor in the last two to three years is now sitting in a market where: public multiples are compressed, strategic acquirers (Microsoft, Salesforce, SAP) are active buyers, and the IPO window for software has become unpredictable. Continuation vehicles and GP-led secondaries in software-focused funds may accelerate as sponsors look for exit paths that don't depend on a fully recovered IPO market.

Second, the private AI-adjacent software companies — the ones like Databricks (data infrastructure, $134 billion) that have positioned themselves as foundational to enterprise AI rather than competitive with it — may be insulated from the broader SaaS narrative entirely. Databricks grew ARR to $3.5 billion, raised $4 billion in December, and its secondary market activity has reflected strong buyer interest. The same logic Thoma Bravo is applying in buyouts maps to how secondary buyers may want to think about the private company stack.

The Counterargument

The bear case on Spaht's analysis isn't that his data is wrong — it's that his incentives are obvious. Thoma Bravo manages $183 billion largely in software assets. Of course they see a buying opportunity. Of course the narrative is "overcorrected."

And there's a structural critique that goes deeper than incentives. The per-seat revenue model is genuinely at risk, and the timeline for AI agent adoption may be faster than most incumbents can adapt to. If the enterprise software budget increasingly flows to foundation model providers and AI infrastructure, traditional application software faces not just slower growth but potential shrinkage — and "zero tolerance for error" workflows are not immune to replacement if AI reliability improves fast enough.

The debate between "cyclical panic" and "structural disruption" is live and has not been resolved.

What Thoma Bravo's analysis adds — regardless of where you come out — is a useful filter. Not all software is the same category of risk. The market has been pricing it that way. The firms writing the largest checks in the space are telling LPs explicitly that the market has it wrong.

📈Data Point of the Day

This Slide:

🎓 Manual

Rule of 40

A benchmark for evaluating software company health, calculated as revenue growth rate plus free cash flow margin. A score above 40 is considered healthy; scores above 60 are exceptional. Introduced as a heuristic for balancing growth and profitability, it has become one of the primary valuation screens used by PE buyers and public market investors evaluating SaaS businesses.

Augment Markets Inc. is a technology company offering software and data services. Brokerage services are offered through Augment Capital LLC, an affiliated broker-dealer and member FINRA/SIPC. Investment advisory services are offered through Augment Advisors LLC, an SEC-registered investment adviser.

Important Disclosures: This material has been prepared for informational purposes only. None of the information provided represents a recommendation, an offer or the solicitation of an offer to buy or sell any security. The information provided does not constitute investment, legal, tax, or accounting advice. You should consult with qualified professionals before making any investment decisions. Investing in private securities involves substantial risk, including the potential loss of principal. Private securities are typically illiquid, have limited pricing transparency, and often require longer holding periods. These investments are available exclusively to qualified accredited investors and offer no guarantee of returns. An IPO or other liquidity event is not guaranteed. Additionally, past performance of private securities does not indicate or predict future results. Share price data are estimates only, based on proprietary data from Caplight and Augment Markets Inc. and its affiliates.

Paul leads editorial at Augment, building Pulse into the private markets' go-to intelligence source. He also develops editorial content strategies for startups and venture capital firms. Previously, he spent 15 years as a business and opinion journalist at The New York Times, Fortune, Fast Company, Reuters, and more. He believes transparency creates liquidity—and that someone should actually publish what private shares are trading for. He lives in Marin with his wife and two rescue dogs, and wishes he had more time to surf.

Learn more

FOR QUALIFIED INSTITUTIONAL AND ACCREDITED INVESTORS ONLY: Under federal securities laws, private market investments on this platform are available exclusively to Institutional and Accredited Investors. Verification of status required before investing. Private investments involve significant risks including illiquidity, potential loss of principal, and limited disclosure requirements. "Augment" refers to Augment Markets, Inc. and its affiliates. Augment Markets, Inc. is a technology company offering software and data services, not a bank or financial institution. Cash Accounts are provided by Modern Treasury Corp. financial institution partners and through Augment's technology. Augment does not act as a money services business, provide money transmission, or serve as a custodian of funds. Funds held in your Cash Account are not FDIC insured unless expressly disclosed. Full terms available in the Augment Cash Account Agreement.Brokerage services are offered through Augment Capital, LLC, an affiliated broker-dealer and member FINRA/SIPC. “Investment accounts” are not brokerage accounts and do not hold customer funds or securities. Investment advisory services are offered through Augment Advisors, LLC, an SEC-registered investment adviser. Registration with the SEC does not imply a certain level of skill or training. Augment and its affiliates do not provide legal or tax advice; consult your attorney or tax professional regarding your specific situation. For additional information, please refer to Augment Advisors, LLC’s Form ADV Part 2A (Firm Brochure) and FINRA BrokerCheck.