.jpeg)

Arizona filed the first-ever criminal charges against a prediction market company, accusing Kalshi of running an illegal gambling operation. Meanwhile, both Kalshi and rival Polymarket are in talks to raise at $20 billion valuations — roughly double where each sat just a few months ago. The collision of criminal exposure and record fundraising ambition tells you everything about where prediction markets are right now.

Thursday Thesis: The Jurisdictional Bet

Prediction markets have a definitional problem.

Are they financial instruments — regulated futures exchanges where price discovery creates real-world informational value? Or are they gambling products — places where people bet money on outcomes they can't influence and probably can't predict?

The answer determines everything: who regulates them, whether they're legal in all 50 states, and ultimately whether their current valuations are justified. And right now, no one agrees.

Arizona made its position clear yesterday. The state's attorney general filed 20 criminal charges against Kalshi, accusing the platform of operating an illegal wagering business and accepting bets on Arizona elections without state approval. It's the first criminal action against a prediction market in U.S. history — and the timing is pointed. The charges landed the same week March Madness kicked off, one of the biggest betting events of the year, and just days after Kalshi launched a $1 billion perfect bracket promotion.

Kalshi's response was predictable: the company argues it's a federally regulated exchange subject exclusively to CFTC oversight, not state gambling law. CFTC Chair Michael Selig — a Trump appointee — backed them up within hours, calling the Arizona charges "a jurisdictional dispute and entirely inappropriate as a criminal prosecution." He added that the CFTC is "evaluating its options," which likely means federal preemption arguments in court.

This isn't just a legal dispute. It's a bet on which definition of "market" prevails.

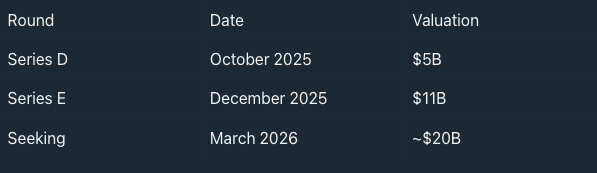

From $2B to $20B in Eight Months

To understand why this fight matters, you have to understand how quickly money has moved into prediction markets.

Kalshi's funding trajectory over the past year:

Polymarket has tracked almost the same arc. Intercontinental Exchange — the parent company of the New York Stock Exchange — committed up to $2 billion to Polymarket at a $9 billion valuation in October 2025. As of this month, Polymarket is reportedly also seeking a $20 billion valuation, per the Wall Street Journal.

The revenue story explains the investor enthusiasm. Kalshi told investors in November that it was on an annualized pace of $600 million to $700 million in net revenue, with some reports now citing a $1 billion to $1.5 billion run rate, per the WSJ. Sacra estimates the company generated $260 million in revenue in 2025 — up nearly 1,000% year-over-year. The engine driving it: sports. Roughly 89% of Kalshi's 2025 fee revenue came from sports contracts, with the NFL season alone generating $138 million in the final months of the year.

That last number matters. Sports betting represents approximately 90% of Kalshi's trading volume — which is precisely what Arizona's attorney general says makes it a gambling operation, not a financial exchange.

Two Platforms, Two Regulatory Strategies

Kalshi and Polymarket have built parallel empires with notably different regulatory postures.

Kalshi is the regulated incumbent. Founded in 2018, it won a landmark legal fight to offer election markets after suing the CFTC under the Biden administration. It operates openly in all 50 states, backed by Sequoia, Andreessen Horowitz, Paradigm, and CapitalG. Trump Jr. serves as a strategic adviser. The company's argument is that its contracts are "event contracts" under the Commodity Exchange Act — a category that preempts state gambling law. More than 20 civil lawsuits from various states test that claim. Arizona's criminal charges are something different: the first attempt to use the threat of misdemeanor convictions and asset forfeiture as leverage.

Polymarket is the offshore-turned-domestic challenger. Founded in 2020 and blockchain-based, Polymarket settled with the CFTC in 2022 for serving U.S. users without authorization and has since operated primarily outside the country. Last year it acquired a derivatives exchange and clearing house, receiving CFTC clearance to re-enter the U.S. market — though its domestic product is not yet fully operational. This makes Polymarket something of a spectator in the current legal fight: it faces no criminal charges, but its ability to compete in the U.S. ultimately depends on the same jurisdictional question Kalshi is fighting.

The irony is that Polymarket — the decentralized, crypto-native platform that was once the regulatory bad actor — may be entering the U.S. market just as its CFTC-regulated rival is taking fire from state attorneys general.

Why the Jurisdictional Fight Is Structurally Unresolved

The core legal question has been producing contradictory rulings in courts across the country. Some federal judges have held that Kalshi's sports contracts are so similar to sports betting that state gaming licenses are required. Others have agreed with Kalshi that federal commodity law preempts state regulation. Legal analysts following the cases note that the Supreme Court may ultimately need to step in to resolve the conflict — which could take years.

In the meantime, the battleground is expanding. Kalshi has preemptively sued Arizona, Utah, and Iowa in federal court to prevent state action. The Arizona federal judge handling that injunction request denied Kalshi's motion for a temporary restraining order Tuesday, even as the criminal charges were being filed — a signal that federal courts aren't automatically deferring to the CFTC's position.

What makes this structurally tricky for investors: the Trump administration's support is real but not permanent. CFTC Chair Selig is the sole sitting commissioner on a five-seat body, with the other four seats still unfilled. A future administration — or a differently composed CFTC — could reverse course entirely. The regulatory tailwind Kalshi is counting on is a policy choice, not a legal mandate.

The Private Markets Angle

Prediction markets aren't currently on Augment's platform, and they're a distinct asset class from the venture-backed secondaries that Augment trades. But the Kalshi and Polymarket regulatory story is worth tracking for two reasons:

First, the valuation trajectory illustrates something your readers see constantly in private markets: a company's fundraising multiple often outruns its legal clarity. Kalshi raised at $11 billion in December while facing more than 20 civil lawsuits. Now it's seeking $20 billion the week after the first criminal charges in its industry's history. Investors are explicitly betting that federal preemption holds — and pricing the risk accordingly.

Second, the definitional fight — what is a "market" versus what is "gambling" — has a direct parallel in private secondary markets. For years, platforms trading private company shares operated in a gray zone, and regulators worked through what rules applied. The resolution of that ambiguity — through FINRA registration, broker-dealer oversight, and ATS designation — is what made platforms like Augment possible. Prediction markets are in an earlier, messier version of that same fight. How it resolves will shape a significant corner of the financial markets landscape.

👀 What We're Watching

- The Arizona criminal case. Misdemeanor charges carry fines of $10,000 to $20,000 — modest for a company of Kalshi's scale — but the real leverage is asset forfeiture and the criminal prosecution framework, which gives Arizona prosecutors subpoena power and investigative tools unavailable in civil litigation. If other states follow with criminal filings, the dynamic changes.

- The fundraising outcome. Both Kalshi and Polymarket pursuing $20 billion valuations simultaneously, in the middle of escalating legal exposure, is either a display of investor confidence in federal preemption or a classic private markets pattern of raising before bad news settles. The timing of these rounds relative to legal developments will be telling.

- Congressional action. Representatives from both parties have introduced legislation that would restrict prediction market contracts on topics including war and sports. A statutory fix would be cleaner than years of litigation — but Washington's record on fintech legislation suggests this could take a while.

Augment Markets Inc. is a technology company offering software and data services. Brokerage services are offered through Augment Capital LLC, an affiliated broker-dealer and member FINRA/SIPC. Investment advisory services are offered through Augment Advisors LLC, an SEC-registered investment adviser.

Important Disclosures: This material has been prepared for informational purposes only. None of the information provided represents a recommendation, an offer or the solicitation of an offer to buy or sell any security. The information provided does not constitute investment, legal, tax, or accounting advice. You should consult with qualified professionals before making any investment decisions. Investing in private securities involves substantial risk, including the potential loss of principal. Private securities are typically illiquid, have limited pricing transparency, and often require longer holding periods. These investments are available exclusively to qualified accredited investors and offer no guarantee of returns. An IPO or other liquidity event is not guaranteed. Additionally, past performance of private securities does not indicate or predict future results. Share price data are estimates only, based on proprietary data from Caplight and Augment Markets Inc. and its affiliates.

Paul leads editorial at Augment, building Pulse into the private markets' go-to intelligence source. He also develops editorial content strategies for startups and venture capital firms. Previously, he spent 15 years as a business and opinion journalist at The New York Times, Fortune, Fast Company, Reuters, and more. He believes transparency creates liquidity—and that someone should actually publish what private shares are trading for. He lives in Marin with his wife and two rescue dogs, and wishes he had more time to surf.

Learn more

FOR QUALIFIED INSTITUTIONAL AND ACCREDITED INVESTORS ONLY: Under federal securities laws, private market investments on this platform are available exclusively to Institutional and Accredited Investors. Verification of status required before investing. Private investments involve significant risks including illiquidity, potential loss of principal, and limited disclosure requirements. "Augment" refers to Augment Markets, Inc. and its affiliates. Augment Markets, Inc. is a technology company offering software and data services, not a bank or financial institution. Cash Accounts are provided by Modern Treasury Corp. financial institution partners and through Augment's technology. Augment does not act as a money services business, provide money transmission, or serve as a custodian of funds. Funds held in your Cash Account are not FDIC insured unless expressly disclosed. Full terms available in the Augment Cash Account Agreement.Brokerage services are offered through Augment Capital, LLC, an affiliated broker-dealer and member FINRA/SIPC. “Investment accounts” are not brokerage accounts and do not hold customer funds or securities. Investment advisory services are offered through Augment Advisors, LLC, an SEC-registered investment adviser. Registration with the SEC does not imply a certain level of skill or training. Augment and its affiliates do not provide legal or tax advice; consult your attorney or tax professional regarding your specific situation. For additional information, please refer to Augment Advisors, LLC’s Form ADV Part 2A (Firm Brochure) and FINRA BrokerCheck.