.jpeg)

Cerebras printed the first true blockbuster tech IPO of 2026 — a 108% first-day pop on a $5.5B raise — and the calendar behind it tells the story of the week. Anthropic is in talks for $30B at a $900B valuation, doubling its February mark. Anduril doubled to $61B in five months. The private market is repricing its top names faster than the IPO window can absorb them.

The Big Story: Cerebras Took the Pop

Cerebras Systems priced its IPO at $185 on Wednesday evening, above a range that had already been raised twice. On Thursday morning it opened at $385 — a 108% pop — and the company raised $5.55 billion on a fully diluted valuation of $56.4 billion. That valuation works out to roughly 110 times trailing 2025 revenue ($510M), a multiple that reflects strong public market demand for AI-inference exposure. Today it settled down about 10%, holding onto much of the initial pop.

The framing matters because Cerebras is the first big AI-infrastructure IPO since the post-2021 reset. Bankers and CFOs spent the spring asking which company would test the window first; Cerebras answered, and the answer was "comfortably." Morgan Stanley, Citigroup, Barclays, and UBS led the book.

What's worth watching is the path back from this print. A 108% first-day pop is a windfall for allocated investors and a flag for the issuer that capital was left on the table. Past mega-pops — Snowflake, Airbnb — turned the next round of issuers more aggressive on pricing rather than more conservative.

Cerebras also enters the public market with concentrated revenue: G42, OpenAI (in a complicated circular relationship), MBZUAI, and AWS make up the customer list. Investors are pricing the inference thesis, not the customer ledger. Whether that thesis survives the lockup is the next story.

Source: TechCrunch · Bloomberg

Anthropic Closes In on $900B

Bloomberg reported Tuesday that Anthropic is in talks to raise at least $30 billion at a valuation north of $900 billion — pre-money. Last week's Thursday edition described how the company's tender priced at $350B while secondary buyers were pricing it closer to $1T. The new round, if it closes at the reported terms, ratifies the secondary print and then some.

The pace is the story. Anthropic last raised in February at $183B post-money. A $900B primary mark would be roughly a 5x step-up in 90 days — faster than OpenAI's recent re-rating from $300B to $852B, and on a revenue base that, while growing, is smaller. Reported figures put Anthropic's enterprise customer count ahead of OpenAI in some segments, and Claude Code revenue has been the cited growth engine in deck materials we've seen referenced publicly.

The structural read: primary capital appears to be following secondary signals, not leading them, which is what happens when the tape is moving faster than allocator memos can be written. For Augment subscribers tracking the Power 20, one key variable to monitor is whether the gap between primary and secondary valuations narrows or widens.

Source: Bloomberg · TechCrunch background

Anduril at $61B, Defense Tech Reset

Yesterday's edition covered this in depth, but the week's arc is incomplete without it. Anduril closed $5 billion at a $61 billion valuation, with Thrive Capital and Andreessen Horowitz co-leading the Series H. That's a doubling of the valuation since the December 2025 round. Havoc — a smaller all-domain autonomy company — added $100M Series A this week, bringing its total to ~$200M raised since 2024.

Read together with Cerebras and Anthropic, the takeaway isn't sector-specific. It's that some of the most-watched private names in three different sectors — AI infrastructure, AI labs, defense — are repricing on roughly the same cadence. Capital is concentrating, not diversifying, and the dispersion between top-decile and median private rounds has rarely been wider.

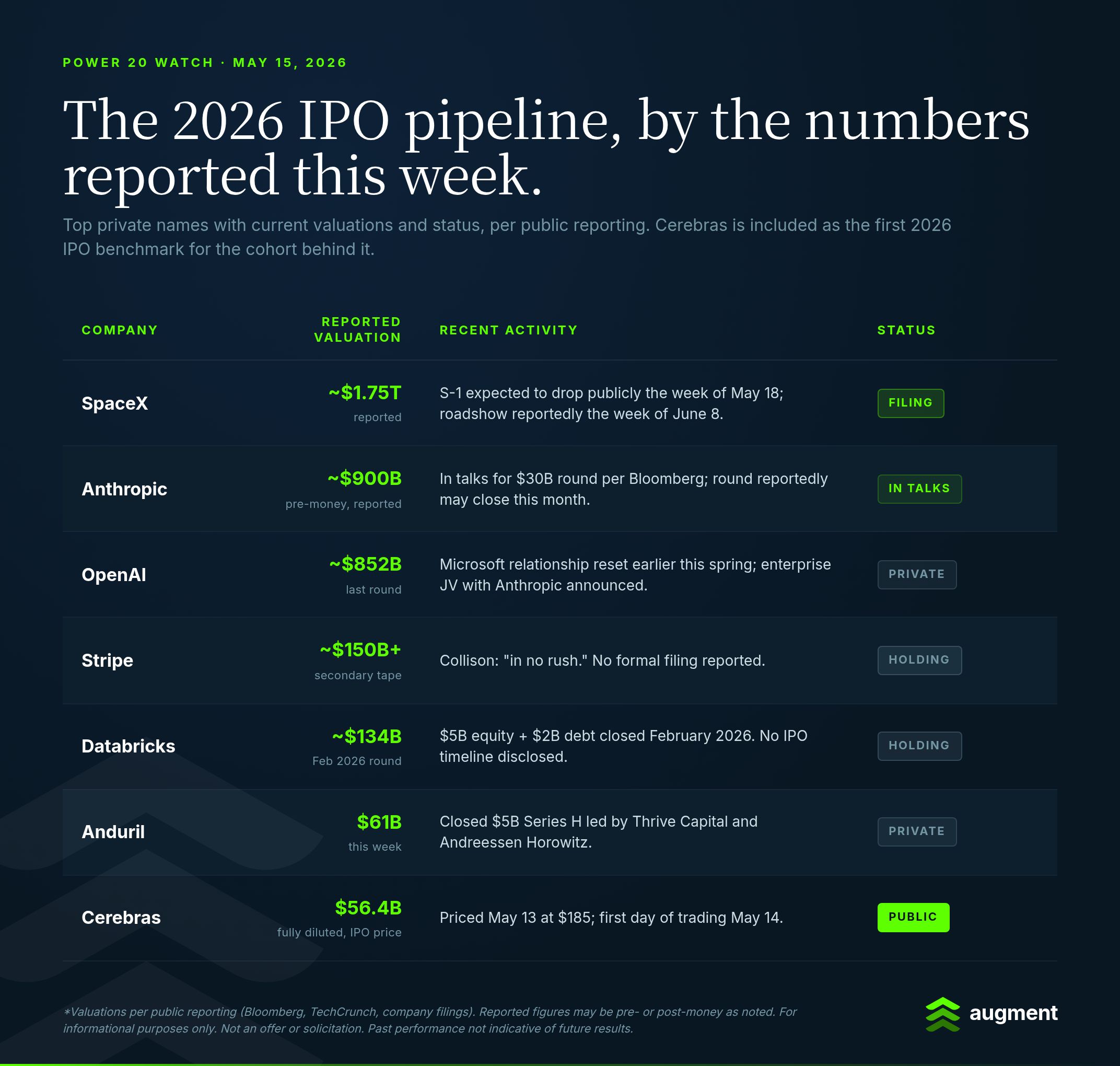

Power 20 Watch

Cerebras' pricing answers one question: The public-market appetite for AI infrastructure is real. Recent private market activity as reported:

The non-obvious read: if SpaceX, Anthropic, and OpenAI all list in 2026, they could raise a reported combined ~$135B between SpaceX and OpenAI alone — more than the entire US tech IPO market raised in 2021 at peak. That capacity question is the real Power 20 story for the rest of the year. The Cerebras pop suggests the pricing was off. Whether it’s the case at $1.75T for a single name is the next test.

💨 Quick Takes

Vapi hits $500M valuation as Amazon Ring picks it over 40 rivals — AI voice startup Vapi closed a $50M Series B led by Peak XV; the Amazon Ring contract was the validation event. Voice is starting to look like the next "every enterprise needs one of these" category.

Blitzy raises $200M at $1.4B for autonomous coding — Northzone-led. Adds to the agentic-software-development cohort alongside Cognition, Cursor, Codeium. Capital is consolidating fast.

Reserv lands $125M Series C from KKR — Insurance claims AI. KKR leading a Series C is the marker for "scaled enough to be PE-adjacent." Worth watching what other late-stage AI verticals get the same treatment.

Parker files for bankruptcy — Reminder that the dispersion in private markets cuts both ways. Cards-for-e-commerce was a 2021-cohort thesis that didn't survive the rate environment.

📈 Data Point of the Day

110x

That's roughly the multiple Cerebras commands at its $185 IPO price against trailing 2025 revenue of $510M, using the $56.4B fully diluted valuation. For context, Nvidia trades at roughly 25x trailing revenue on the public tape today. The premium is the price of being a pure AI-inference vehicle in a market starved of them.

🎓 Manual

Fully Diluted Valuation

A company's valuation calculated as if every outstanding security — common shares, preferred shares, vested and unvested options, warrants, and convertible debt — were converted into common stock at once. It's the bigger of the two numbers usually quoted (the other being post-money, which counts only issued shares plus the new primary). Cerebras' "$56.4B" headline is fully diluted; the equivalent on issued-share basis is meaningfully lower. When private-market valuations are reported, "fully diluted" usually flatters the comparison.

👀 What We're Watching

- SpaceX's S-1. Public filing reportedly expected the week of May 18, with an institutional roadshow the week of June 8. A reported $1.75T valuation would make this the largest IPO in history. The Cerebras pricing experience will be referenced in every banker meeting on this deal.

- Starship Flight 12. Targeted for May 19. Twelfth integrated test of the full stack and the debut of next-generation Super Heavy and Raptor hardware. SpaceX is reportedly $15B+ into the program. A clean flight changes the operational narrative going into the S-1 roadshow.

- The Anthropic close. Bloomberg's sourcing suggests the $30B round could close by month-end. If it prices materially above $900B pre, secondary marks could reprice to the new valuation.

- The Korean and European tape. A reminder that the AI-infrastructure story isn't only American. SK Hynix and Samsung memory dynamics, and European labs like Mistral and Aleph Alpha, are setting up second-order trades that the US-centric coverage misses.

Augment Markets Inc. is a technology company offering software and data services. Brokerage services are offered through Augment Capital LLC, an affiliated broker-dealer and member FINRA/SIPC. Investment advisory services are offered through Augment Advisors LLC, an SEC-registered investment adviser.

Important Disclosures: This material has been prepared for informational purposes only. None of the information provided represents a recommendation, an offer or the solicitation of an offer to buy or sell any security. The information provided does not constitute investment, legal, tax, or accounting advice. You should consult with qualified professionals before making any investment decisions. Investing in private securities involves substantial risk, including the potential loss of principal. Private securities are typically illiquid, have limited pricing transparency, and often require longer holding periods. These investments are available exclusively to qualified accredited investors and offer no guarantee of returns. An IPO or other liquidity event is not guaranteed. Additionally, past performance of private securities does not indicate or predict future results. Share price data are estimates only, based on proprietary data from Caplight and Augment Markets Inc. and its affiliates.

Paul leads editorial at Augment, building Pulse into the private markets' go-to intelligence source. He also develops editorial content strategies for startups and venture capital firms. Previously, he spent 15 years as a business and opinion journalist at The New York Times, Fortune, Fast Company, Reuters, and more. He believes transparency creates liquidity—and that someone should actually publish what private shares are trading for. He lives in Marin with his wife and two rescue dogs, and wishes he had more time to surf.

Learn more

FOR QUALIFIED INSTITUTIONAL AND ACCREDITED INVESTORS ONLY: Under federal securities laws, private market investments on this platform are available exclusively to Institutional and Accredited Investors. Verification of status required before investing. Private investments involve significant risks including illiquidity, potential loss of principal, and limited disclosure requirements. "Augment" refers to Augment Markets, Inc. and its affiliates. Augment Markets, Inc. is a technology company offering software and data services, not a bank or financial institution. Cash Accounts are provided by Modern Treasury Corp. financial institution partners and through Augment's technology. Augment does not act as a money services business, provide money transmission, or serve as a custodian of funds. Funds held in your Cash Account are not FDIC insured unless expressly disclosed. Full terms available in the Augment Cash Account Agreement.Brokerage services are offered through Augment Capital, LLC, an affiliated broker-dealer and member FINRA/SIPC. “Investment accounts” are not brokerage accounts and do not hold customer funds or securities. Investment advisory services are offered through Augment Advisors, LLC, an SEC-registered investment adviser. Registration with the SEC does not imply a certain level of skill or training. Augment and its affiliates do not provide legal or tax advice; consult your attorney or tax professional regarding your specific situation. For additional information, please refer to Augment Advisors, LLC’s Form ADV Part 2A (Firm Brochure) and FINRA BrokerCheck.